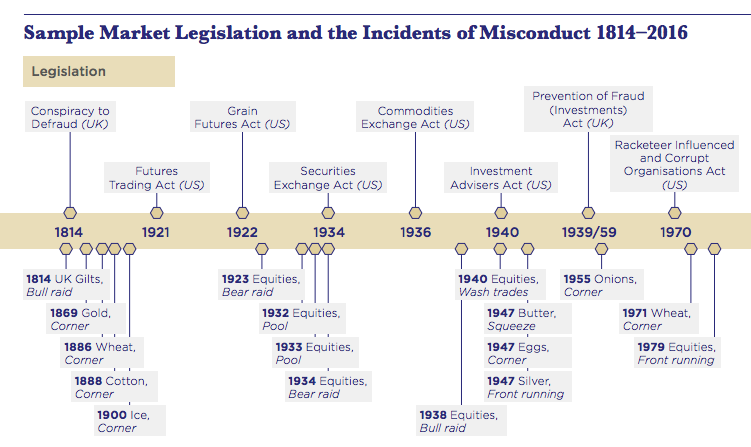

- FICC Markets Standards Board analysed 200 years of enforcement cases, reviewing 400 cases from 19 countries.FMSB report found 26 common types of market misconduct, including insider trading and spoofing.The data is “a history of human greed,” according to FMSB Chair Mark Yallop.All 26 ways are listed below.

LONDON – For as long as there have been markets, there have been participants trying to gain an illegal edge.

The FICC Markets Standards Board (FMSB), the industry body overseeing standards in fixed income, currency and commodity trading, compiled a database of legal cases stretching back 200 years to try to understand the root causes of this market misconduct.

FMSB Chair Mark Yallop called the data “a history of human greed.”

The analysis done by the FMSB, the first of its kind, reviewed over 400 enforcement cases from 19 countries, over a 200 year period, to identify behavioural patterns in market manipulation. Although they stopped at just over 400 cases, says Yallop, they “could have gone to 4,000.”

There were 250 cases between 2000 and 2017 alone.

Here's a timeline of just some of those:

According to Yallop, they found "relatively few common causes," but 26 types of behavioural misconduct, which repeat and recur over time.

These behaviours are "jurisdictionally and geographically neutral," and cut across asset classes. "This is rational," says the report, since "asset classes do not generate conduct risks - people do."

The patterns were also found to be "strikingly similar" to those found by the US Senate Committee in 1934, in its investigation into the causes of the 1929 Wall Street Crash - suggesting that malpractice has changed little.

Mark Steward, a senior UK market enforcement official, highlighted a case from over 100 years ago. In 1878, he said, the directors of the City of Glasgow bank were investigated, convicted and jailed for fraud, all in the space of a few months.

Comparing this to the speed and efficiency of current practices, he said, "where did we go wrong?" at a conference in London on Wednesday.

Patterns of behaviour

The FMSB's report calls for a "new and additional approach to the conduct problem." Despite existing rules and regulations, it says, "misconduct has not only continued, but the same patterns of behaviour have repeated and developed."

It gives the example of the Myanmar stock exchange, which had been open for just 16 weeks, and had listed only two stocks, before it issued its first warning against "spoofing" - when traders trick the market into thinking there's more demand to buy or sell than there actually is - in 2016.

Spoofing is one of the 26 types of misconduct the report identifies, alongside "wash trades," when traders buy and sell the same securities at the same time move money, "ramping," when traders artificially raise or depress the market price of securities, and insider trading.

Although electronic trading has improved transparency and auditability, says the report, market abuse cannot be "coded out." New technologies have come with potential new vulnerabilities, which are "growing in scale."

The increasing use of online trading systems, for example, risks unauthorised individuals logging on, either using false identities or by stealing the identities of legitimate traders.

New concerns have prompted the development of new controls, such as "kill switches," which cut off trading when pre-set limits are breached, and "speed bumps," which slow down trading by introducing microsecond delays.

An increase in investigations

According to Steward, there was a 75% rise in the number of FCA investigations into suspected wholesale or markets misconduct begun in the last year. This was aided by legislative changes introduced by the Market Abuse Regime (MAR), he said: "MAR has extended the scope of the reporting regime," resulting in "more participants reporting more data."

Steward also mentioned lawyer Andrew Green QC's assessment that the FCA had been misguided in its judgment that further investigations into the failure of HBOS would not have been successful, and were therefore not done.

"While there is little doubt that 'prospects of success' is an important element in considering whether enforcement resources should be deployed, I think it must be right that the merits of a case cannot be assessed before you have the relevant evidence, or even the key evidence," he said.

But, he said, Green's points had "prompted some thinking around what should be the starting point for an investigation." Weighing in on the problem at the AFME conference, Linklaters Partner Martyn Hopper said the world had "become a more complex place," which "poses problems, including for prosecutors."

Continued malpractice, says FMSB's report, is partly due to "the frailty of collective memory," as past scandals get further away. But both principles-based and rules-based regulation "struggle to address the causes of conduct failure."

What is also clear, says the report, is that "the lessons learnt by one firm or one generation do not necessarily pass to the next."

The 26 ways to cheat the market:

Pools: marketing campaigns and pre-arranged transactions organised by a group, to give a false impression of market activity or to ramp up prices. Wash trades: when traders buy and sell the same securities at the same time move money. Wash trades (fraud): when wash trades are used to illicitly transfer money from one account to another. Matched trades: a type of wash trade between two parties, brokered by a third party. Compensation trades / money passes: a type of wash trade between two parties to enable a cash payment to one party. Crosses: when buy or sell orders from the same stock are offset without recording the trade. This also occurs when a broker executes both a buy and sell for the same security from one client to another, where both accounts are managed by the same person. Closing prices: deliberately buying or selling securities and/or derivatives contracts at the close of the market to alter the closing price. Reference prices, fixes: deliberately buying or selling securities and/or derivatives contracts at or around the time that the reference prices are set, to influence them. Ramping: when traders artificially raise or depress the market price of securities. Spoofing: when traders trick the market into thinking there's more demand to buy or sell than there actually is. Layering: entering a sequence of orders at increasingly higher or lower prices to ramp or depress market prices. Squeeze / corner: when a party does not seek dominance but attempts to gain control of sufficient amounts of a commodity or security to impact prices. New issue / M&A patterns: attempts to support or increase the price of newly issued securities. Parking / warehousing: selling securities with the agreement that they will be re bought by the seller at a time and a price which means the economic risk of the securities never transfers from the seller. Execution conflicts: when confidential information is disclosed through networks to trading operations, who then either front run or execute against client orders. Front running: when a broker trades an equity in their personal account based on advanced knowledge of pending orders, and profiting from the knowledge. Client information: exploiting knowledge of client information for personal or the firm's gain. Rumours - Bull / bear raids: taking a position in a security, publishing false information and closing the position once the security price has reacted to the information. Insider - Market: using inside and non public information about the market to make trades. Insider - Corporate / advisor: using inside and non public information from an official advisor to make trades. Insider - Relationships / groups: using inside and non public information from a friend or acquaintance to make trades. Cherry picking: executing a client order but withholding the allocation to the client until it is clear whether it will be a winning or losing trade. If the price moves positively, the trade is taken by the firm or trader for their personal account. Portfolio trades - pre hedging: making a trade for the firm's benefit before carrying out a trade for a customer, using information provided by the customer. Window dressing: improving the appearance of a fund's performance before presenting it to clients or shareholders, normally near the end of a year or quarter. Fund managers sell stocks with large losses and buy high-flying stocks, and reporting securities as part of the fund's holdings. Soundings: communicating information before a transaction is announced to one or more potential investors to gauge their interest in a possible transaction and the conditions relating to it, such as potential size or pricing. MNPI disclosure / research: benefiting from using material non-public information (MNPI).