When it comes to boosting stock prices, few things are more important than the willingness of companies to invest in themselves.

With that in mind, bullish investors will be pleased to know that corporate capital expenditure is picking up.

Non-residential fixed investment – spending on things like machinery, factories, and commercial real estate – is up 3.1% on a year-over-year basis, according to Strategas Research Partners.

And while much has been made about the importance of consumer spending in the economy, Strategas argues that it’s less important than capex when it comes to share prices.

Consumer staples and discretionary companies account for 21.6% of the market cap of the Standard & Poor’s 500. Industrial and technology companies, which would be the biggest beneficiaries of more business spending, make up about one-third of the S&P 500, so they’ll play a larger role in pushing the index higher.

"While the consumer, measured in economic terms, may be doing OK, index gains will be far more reliant on investment," Nicholas Bohnsack, co-founder and head of quantitative research at Strategas, wrote in a recent note.

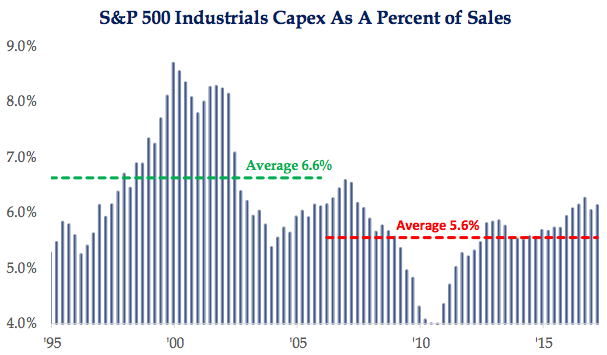

Bohnsack notes that capex for industrials, in particular, has room to expand. Over the last decade or so, companies in the industry have spent less on internal investments than they did over the previous 10 years.

The possibility for higher capex in industrials may be the catalyst the sector needs to maintain the torrid gains it's seen since the US presidential election.

The group surged as much as 14% in the four months after the election on expectations that the $1 trillion of infrastructure spending proposed by President Donald Trump would boost bottom lines. But it's since struggled to break higher amid skepticism that Trump will be able to implement his suggested policies any time soon, if at all.

As for the tech sector, the potential for future gains is driven as much by companies in other industries sinking money into technological advancement as it is by capex spending within the sector. A large part of that will be driven by bigger paychecks for US workers, according to Wells Fargo Funds chief equity strategist John Manley.

"If managers see wages being forced higher, they're going to have to force productivity higher, because they don't think they can price it away," Manley said in an interview earlier this month. "That means they're going to spend more on technology, so they can pay their workers more because the workers can produce more."