Even amid the rise of so-called robo-investors and passive strategies, good old-fashioned stock pickers are continuing to prove their worth.

About 54% of large-cap mutual-fund managers are beating their benchmarks in 2017, the highest-ever success rate at this time of year, according to Bank of America Merrill Lynch data going back to 2009. If they keep up the pace through the end of the quarter, it would be the first year since 2007 – right around the time of the financial crisis – that more than half of them outperformed benchmarks, according to the data.

It’s been an impressive stretch by any measure for investors who make their living analyzing company fundamentals and betting on single stocks. And it’s been a somewhat surprising development amid the rapid growth of passive investment – which often involves computerized and price-insensitive trading.

It wasn’t supposed to be like this. To hear doomsayers tell it over the past several years, the rise of the machines was supposed to hurt active managers. Exchange-traded funds were supposed to homogenize the market, causing stocks to trade increasingly in lockstep.

In reality, the opposite has happened.

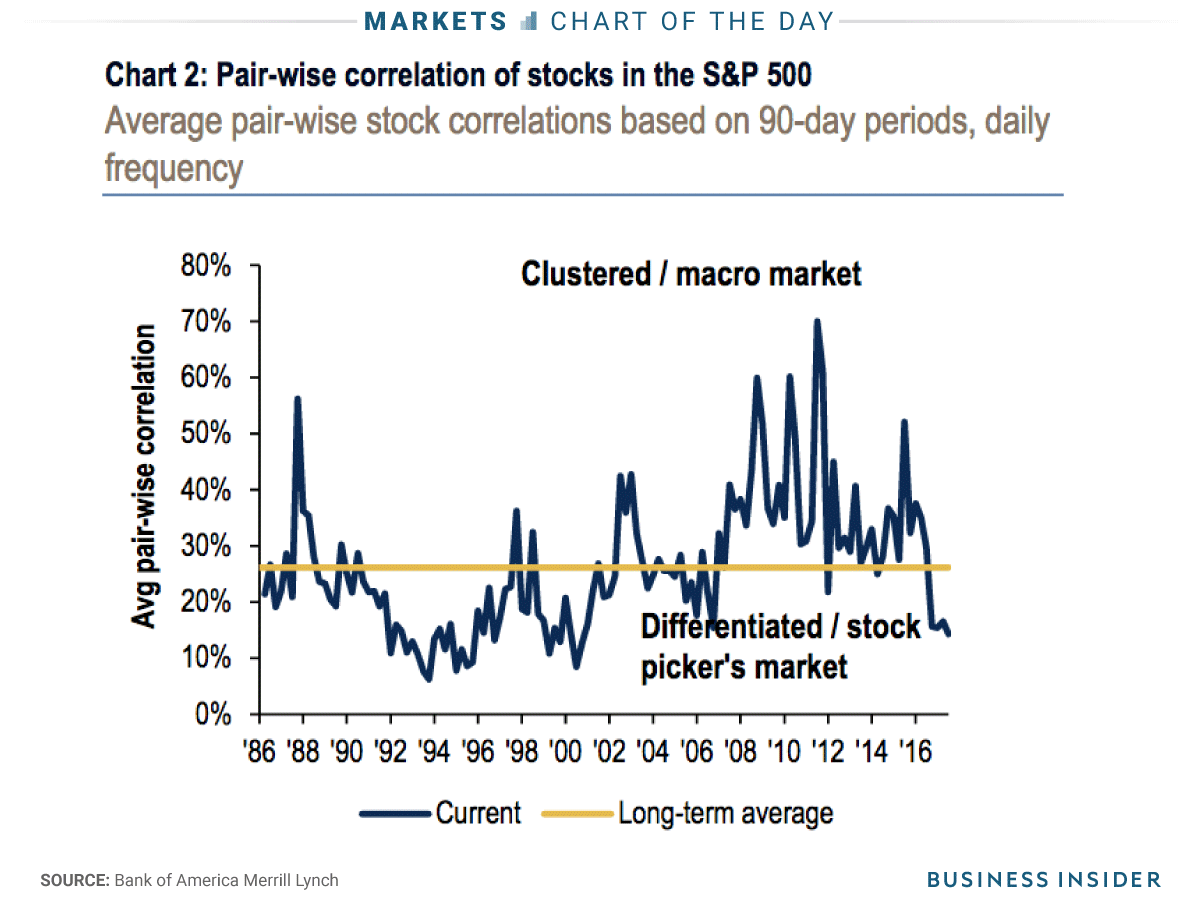

At the root of the resilience has been the average pair-wise correlation of stocks in major indexes - which measures the degree to which they trade in tandem. For the benchmark S&P 500, the measure sits at its lowest since the tech bubble, while companies in the Russell 2000 gauge of small-cap stocks are trading the most independently since 2003, according to BAML data.

BAML attributes active mutual fund managers' outperformance to their being overweight the right sectors. The firm points out that those investors are 96% overweight internet and direct marketing retail stocks, relative to the S&P 500 - and that area has surged year-to-date.

It remains to be seen how well active fund managers will fare once intrastock correlations rebound from current lows. But until then, stock pickers are making the most of their opportunity to show they still matter.