- The International Monetary Fund’s latest Financial Stability Monitor points to lurking market risks that are not on the radar of most Wall Street investors.

- “The current economic environment remains favorable, but short-term risks to global financial stability have increased in the past six months,” the Fund says.

- Key risks include a record pile of leveraged corporate lending, external debt issues for emerging markets, and European banks’ reliance on volatile sources of short-term dollar funding.

Wall Street’s raging post-tax cut enthusiasm has been moderated along with expectations for economic growth, but there are few investors or policymakers expecting any sort of downturn soon.

Naturally, there are pockets of concern like rising bond yields and the prospect of trade wars that pop up now and then and cause ructions in the markets. However, traders are also largely ignoring less prominent sources of risk, three of which are identified in the International Monetary Fund’s latest Financial Stability Monitor.

“The current economic environment remains favorable, but short-term risks to global financial stability have increased in the past six months, as a result of a spike in stock-market volatility in February and continuing investor concerns about rising geopolitical and trade tensions,” Tobias Adrian, a former New York Fed economist who is now director of the IMF’s Capital Markets Department, wrote in a blog accompanying the flagship report released last month.

“Looking ahead, the odds of a downturn remain elevated, and there’s even a small chance of a global economic contraction over the medium-term,” Adrian added, sounding substantially less optimistic than the Wall Street consensus.”Given current financial conditions, risks to financial stability and growth are high over the medium-term.”

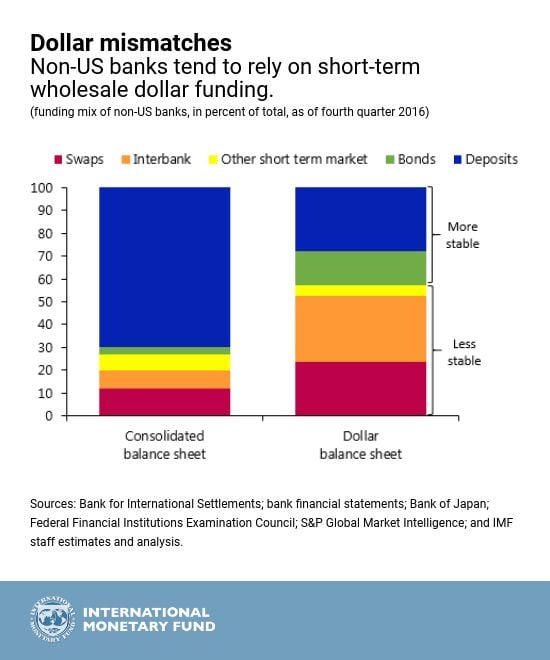

The report flags three "areas of vulnerability": weakening credit quality; external debt-related issues in emerging markets and low-income countries; and dollar liquidity troubles for non-US banks.

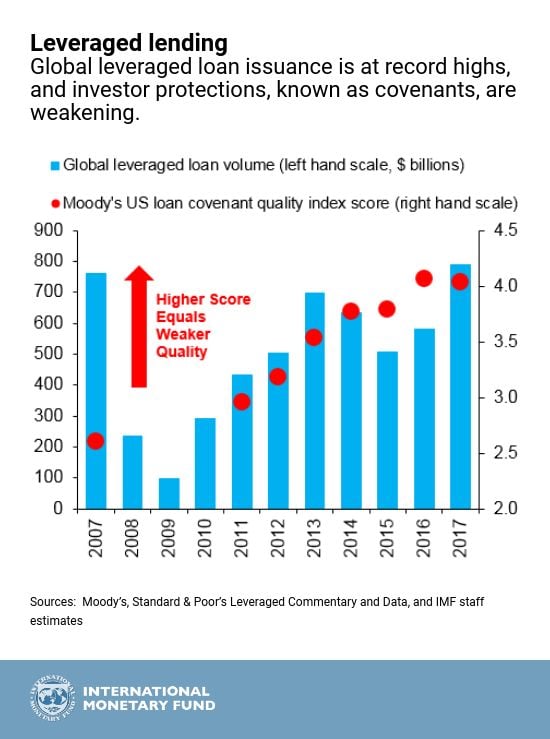

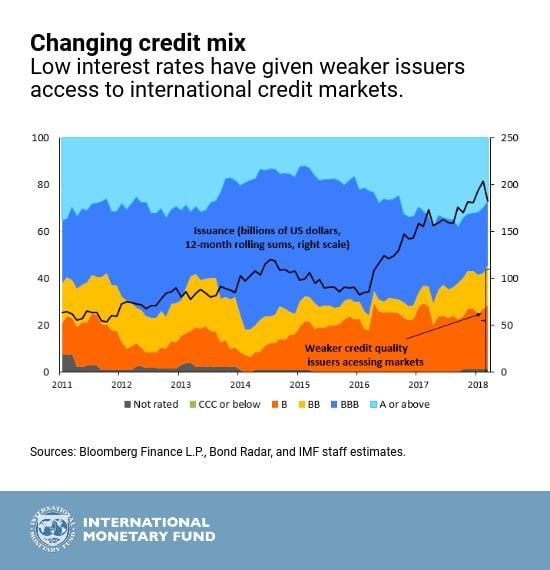

"Increasingly, less creditworthy companies are able to borrow in financial markets," Adrian said. "Global issuance of so-called leveraged loans - made to riskier companies and those with high debt loads - rose to a record $788 billion last year. There are similar trends in corporate bond markets, where lower rated US and euro-area companies account for a growing proportion of bonds."

Another key trouble spot may sound all too familiar to students of emerging-market crises. Low interest rates have allowed countries to take on large amounts of external debt, which leaves them open to the risk of wild currency swings among other factors.

"As the global liquidity tide recedes, flows to emerging markets could decline by as much as $60 billion a year, equal to about a quarter of annual totals in 2010-2017," he said. "In such a scenario, less creditworthy borrowers may experience relatively larger outflows. Low-income countries may be affected, because more than 40% of them are at a high risk of debt distress."

The third potential hit could come from major overseas banks, which the Fund says rely on short-term or wholesale sources for 70% of their funding.

"These dollar liabilities are not always evenly matched with dollar assets in terms of size or maturity," Adrian wrote. This could leave banks exposed to dollar funding problems in the event of a sudden tightening in financial conditions and strains in markets."