Federal Reserve officials have spoken in such hawkish unity in recent days that financial markets have raced to price in a March interest-rate hike, until recently viewed as a low-probability event.

Wall Street was most swayed by a tone of optimism from the New York Fed president, William Dudley, whose permanent vote on the policy-setting Federal Open Market Committee fuels the perception of greater influence at the table.

“I think the case for monetary-policy tightening has become a lot more compelling,” Dudley, a former Goldman Sachs partner, told CNN in a Tuesday interview.

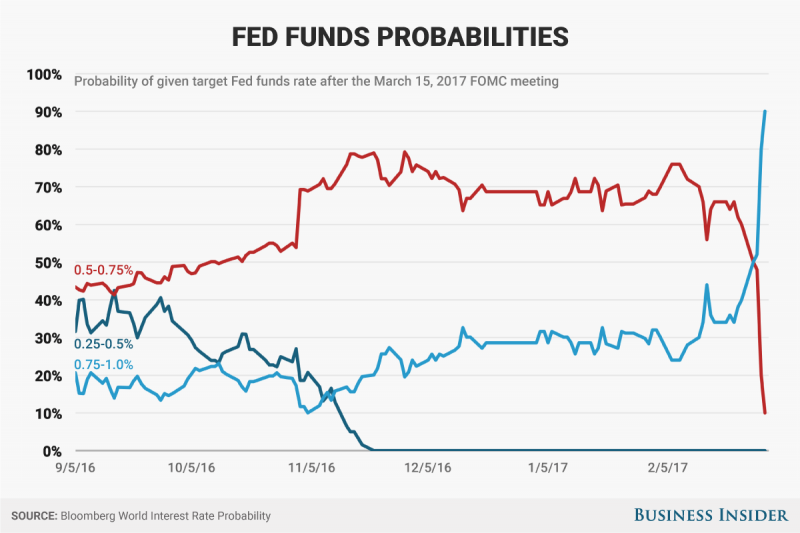

Dudley did not give a specific time for the next move, but his colleagues did. That helped push up market-perceived chances of a March increase up to about 80% from below 40% just last week.

But another trend in the Treasury market is telling: Traders aren’t pricing in more rate increases, simply moving forward the timing of the next move. This suggests bond-market investors don’t believe the stock market hype about the sudden prospect for a burst of economic growth.

The Fed has raised interest rates just twice in the past decade, having brought them to zero during the depths of the Great Recession, in late 2008. But the loose monetary policy has been well justified by weak economic conditions, including a job market that has taken a long time to return to full health and inflation that remains persistently below the Fed’s 2% target. This softness has been reflected in the all to gradual rise in workers’ wages, something that compromises the key US economic engine that is consumer spending.

Now that the central bank appears closer to its goals, policymakers are warming up to moving rates up sooner.

Here's why that would be a big mistake.

A mistake

One clear but unspoken reason for the Fed's change of tune, which has shifted market forecasts of a June rate rise to this month, is a seemingly unstoppable stock market, which seems to be underwriting the policy proposals of President Donald Trump. But there are a lot of ifs in Trump's policy agenda and therefore a lot of reasons to be skeptical of the market's recent record-breaking steak of euphoria.

For one thing, Trump's advisers seem much more focused on trade and immigration issues, where Wall Street has its share of qualms with the Trump camp, than the corporate and individual tax cuts that have investors salivating.

At the same time, the Republican Party can't seem to find consensus on its top stated priority, replacing President Barack Obama's healthcare law. If they fail there, political momentum will swing against them, making things like corporate tax reform and any sort of fiscal stimulus difficult to pass through Congress.

The markets also seem to be vastly overstating the potential for a large fiscal stimulus.

The markets also seem to be vastly overstating the potential for a large fiscal stimulus.

Despite talk of $1 trillion in infrastructure spending, critics suspect much of that will come in the form of subsidies to private firms that are punitive to consumers rather than stimulative. In other words, taxpayers could end up paying to build a private toll road that will then turn around and charge them tolls. No extra disposable income there, negating any potential boost to overall economic growth.

Yet here was Dudley's take on matters: "Since the election we've seen very large increases in household and business confidence, we've seen very buoyant financial markets - the stock market is up, credit spreads are narrow. And we have the expectation that fiscal policy will probably move in a more stimulative direction."

How can he be so sure? And is policy action warranted on the mere hint of a possibility? At the same time, the potential for higher rates from an increasingly motivated Fed could create financial instability and would certainly ratchet up the cost of any new federal spending.

The central bank does not appear to be taking that factor into account just yet.