The investing world is coming to terms with the election of Donald Trump, and all that it might mean for currencies, stocks, and bonds.

And as big investors and bank strategists look ahead to 2017, an emerging theme is the possibility of a global dollar shortage in the near future.

The dollar has strengthened since Trump’s victory, and that could put global companies that borrowed in dollars in a difficult position. Not only is it harder to repay the debt, but it’s also harder to roll over loans when they come due.

“As non-US borrowers struggle to roll a gigantic stock of USD-denominated debt, the cross-currency complex will be a channel of stress,” Societe Generale said in a 124-page opus on the outlook for the fixed income markets.

The French bank added:

"The financial sector may have de-leveraged following the Great Financial Crisis (GFC), but the non-financial sector (government, corporations, households) has not. Needless to say, rising yields will make it harder to roll the debt (e.g. for US high yield borrowers).

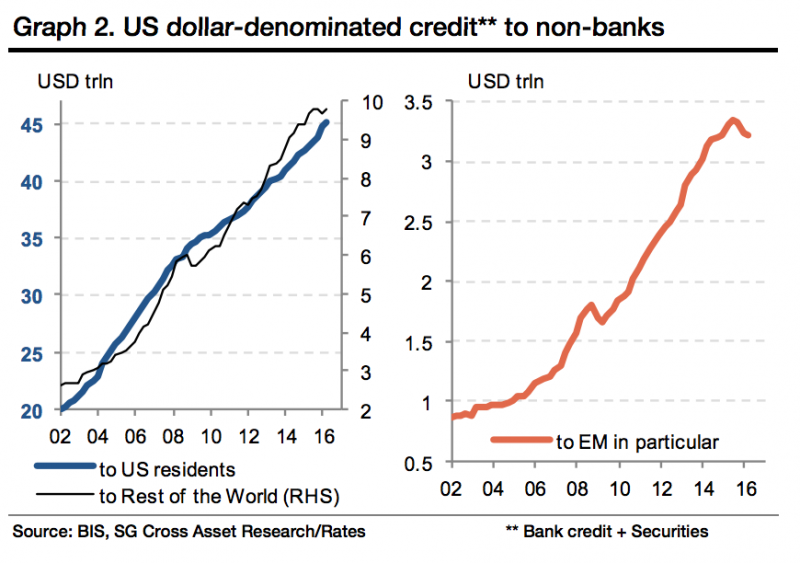

"The challenge looks even fiercer for non-US borrowers who have borrowed in USD (dollar strength will make it harder to repay the debt). There are plenty of them, as the outstanding of USD-denominated credit to the rest of the world has more than doubled over the past 10 years to nearly USD 10trn."

Here's the chart showing that spike in US dollar-denominated credit:

Emerging-market countries and companies have been especially active in their dollar borrowing, currently owing $3.2 trillion in dollar-denominated debt. A little more than half of that comes from banks, with the rest borrowed from the market. That's something in the region of $1.7 trillion in dollar-denominated bonds.

That's all fine and dandy when interest rates in the US are low and currencies are relatively stable. But when the US dollar strengthens and the Federal Reserve looks ready to raise interest rates, there's the potential for a powerful cross-currency effect that could make financing much more difficult for these companies.

Societe Generale pointed to a recent report from the Bank for International Settlements looking at the dollar, bank leverage, and currency markets. In short, when the dollar strengthens, financing conditions tighten. The note said (emphasis ours):

"A key finding is that banks are less keen to lend US dollars to non-US borrowers in periods of strong USD; this is a major concern given the need for non-US borrowers to roll very large amounts of US dollar-denominated debt. Also, USD strength tends to imply a fall in international reserves, hence a diminishing supply of dollars in global markets. All in all, USD scarcity could become a major concern again in 2017, and more so as the Fed continues to be re-priced higher."

Larry Cofsky and Daniel Hochman at Bridgewater Associates, the world's largest hedge fund, highlighted similar risks in a note to clients. They said that while Trump's protectionist trade policies may hit US trading partners, changes in dollar-financing conditions are likely to have a far more meaningful effect in the short term.

The note said:

"As we see it, there are first-order impacts primarily from Trump's proposed protectionist policies, but there will also be second-order impacts, particularly through changes in global dollar liquidity and financing conditions as Trump's policies are discounted in markets. These market conditions will in turn change the incentives for capital flows, which will have subsequent consequences. At this time, the second-order impacts appear to be bigger and clearer than the first-order impacts."

It is still early days following the election of Trump, and policy and markets could go in a whole bunch of different directions. But this looks like an interesting topic to keep an eye on.