Stocks are operating with a mind of their own to an extent not seen since the dotcom bubble.

Normally tossed and turned by geopolitical events and macroeconomic developments, stocks are exhibiting a historically high degree of independence at a time when price swings remain locked near all-time lows.

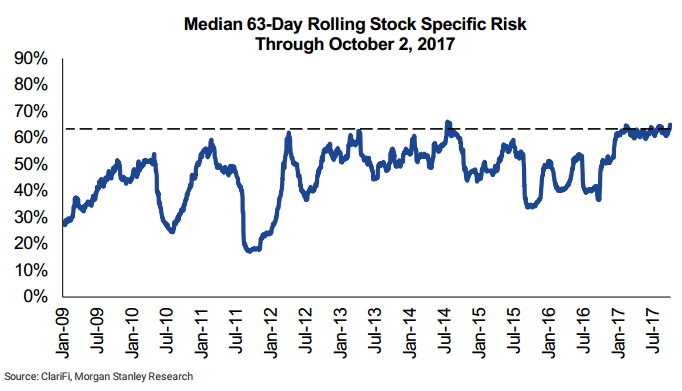

As of earlier this month, 65% of the risk associated with the average S&P 500 stock was inexplainable by a set of six macro risk factors maintained by Morgan Stanley over the past 63 days. That’s the highest since the financial crisis, the firm wrote in a client note.

And if you extend the period of comparison to 252 days, the measure of stock-specific risk is the highest since 2001, the age of the dotcom bubble, Morgan Stanley data show.

These types of market conditions are ideal for stock pickers, who make their living analyzing company fundamentals and betting on single stocks.

About 54% of large-cap mutual-fund managers are beating their benchmarks in 2017, the highest-ever success rate at this time of year, according to Bank of America Merrill Lynch data going back to 2009. If they keep up the pace through the end of the quarter, it would be the first year since 2007 - right around the time of the financial crisis - that more than half of them outperformed benchmarks, according to the data.

At the root of the resilience has been the average pair-wise correlation of stocks in major indexes - which measures the degree to which they trade in tandem. For the benchmark S&P 500, the measure sits at its lowest since the tech bubble, while companies in the Russell 2000 gauge of small-cap stocks are trading the most independently since 2003, according to BAML data.

Stocks won't trade this independently of macro factors, nor other companies, forever. So, more than anything, it's important for active managers to strike while the iron is hot.