In a stock market devoid of big price swings, you can only bet on low volatility for so long.

At a certain point, there are diminishing returns to that approach because measures of volatility can only get so low. Not to mention the investment public eventually catches on to the trade.

With realized volatility on the S&P 500 sitting close to the lowest since 1966, what you should be doing instead is buying stocks that offer the best risk-adjusted return going forward, says Goldman Sachs.

Maximizing risk-adjusted return is another way to describe reaping the biggest gain for the least possible risk. And while this should seem like the obvious end goal for any investor, the firm notes that traders have instead narrowed their focus to minimizing volatility, which they think is an incorrect approach in isolation.

Of course, in a market that’s seen stocks rise gradually for the better part of eight years, there’s also the matter of beating the underlying benchmark. After all, how worthwhile is an investment strategy if it underperforms the S&P 500, in which investment has never been easier?

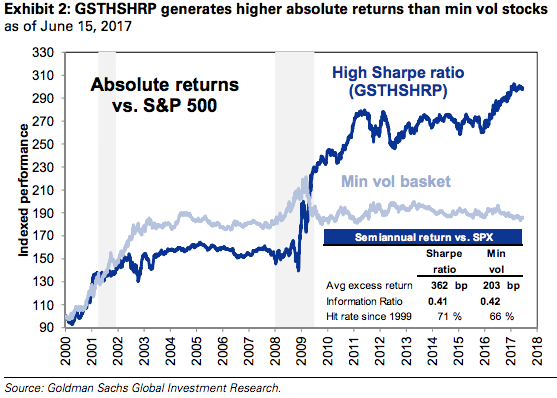

Enter the Sharpe Ratio, which is used to identify risk-adjusted returns on investment. Goldman has used it to pick the best bets in a low-volatility environment, constructing a basket of 50 stocks expected to have high Sharpe Ratios going forward.

The group, which spans all 11 main S&P 500 industries, includes companies ranging from FootLocker to JPMorgan and Intel. And it works.

"Many investors are focused on the wrong objective," Goldman chief US equity strategist David Kostin wrote in a client note. "Fund managers should seek to maximize prospective risk-adjusted returns rather than minimize realized volatility."

Since 1999, Goldman's high prospective Sharpe Ratio basket has beaten strategy wagering on low volatility by a median of 84 basis points, on a rolling six-month absolute basis, Goldman data show.

That dynamic of outperformance gets even more pronounced when the market has been sapped of price swings, similar to what's happening right now. The high Sharpe Ratio index has beaten the low volatility strategy on both an absolute and relative basis so far this year, according to the data.

There's just one catch to this investment method: it doesn't contain any of the so-called FAAMG stocks - Facebook, Amazon, Apple, Microsoft, Google/Alphabet - that have been so responsible for stock gains in recent months.

As such, any investor considering the high Sharpe Ratio approach must ask themselves if it's worth foregoing ownership of some of the stock rally's biggest contributors.

Meanwhile, Goldman is sticking to its strategy.

"We expect our high Sharpe Ratio basket will outperform both low volatility and the S&P 500 on an absolute and risk-adjusted basis during 2H if a low volatility regime persists as is predicted by the term structure," Kostin wrote. Here's a list of some of the stocks Goldman picked - those with expected Sharpe ratios greater than 1.0:

- Anadarko (Sharpe Ratio: 2.1) Range Resource (1.9) Cimarex Energy (1.8) Mallinckrodt (1.4) Tractor Supply (1.3) Foot Locker (1.3) Discover Financial Services (1.2) Mylan (1.2) Kroger (1.1) O'Reilly Automotive (1.1) Snap-on (1.1) Viacom (1.0) AutoZone (1.0) Pfizer (1.0) Biogen (1.0) Quanta Services (1.0) Nucor (1.0)