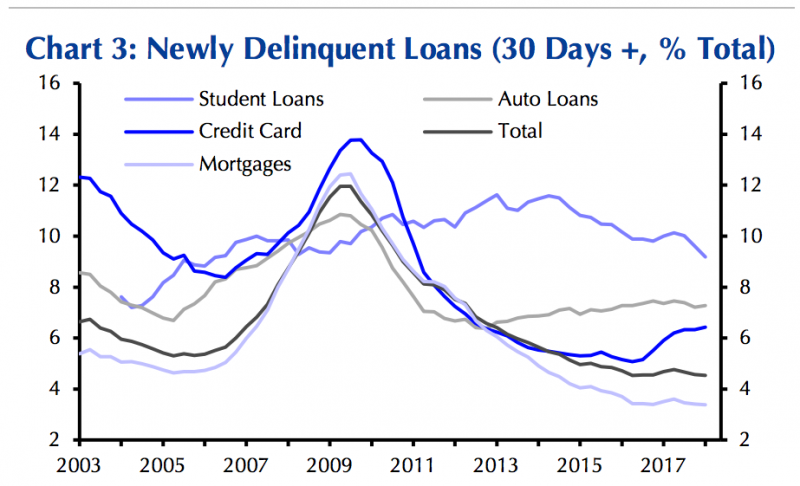

- Late payments on credit-card debt remain on the rise.

- This contrasts with the trend in other forms of credit, including auto loans and mortgages, where late payments of 30 days or more are on the decline.

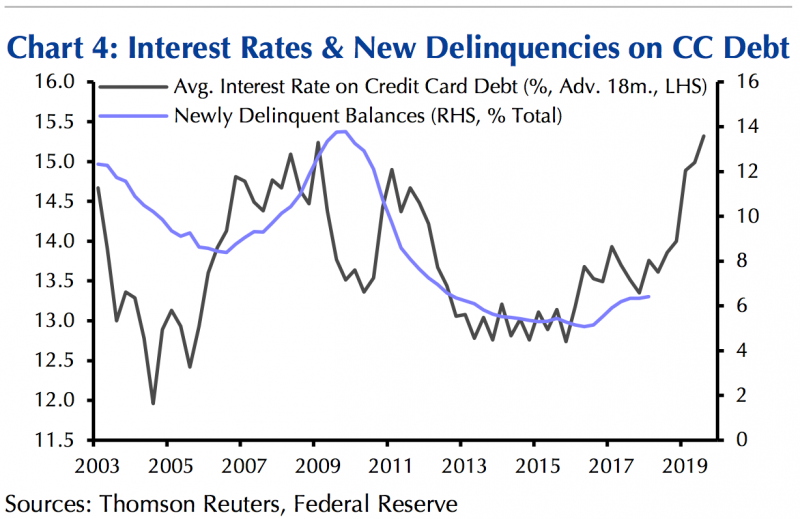

- Michael Pearce, an economist at Capital Economics, said higher interest rates had left more families struggling to pay promptly.

- Paying off credit-card debt on time is one of the most important ways to maintain a good credit score.

It’s getting more expensive to borrow from banks in America, and some credit-card holders are struggling to keep up.

Interest rates, which influence the cost of borrowing, are on the rise after the Federal Reserve kept them near zero for years. That period of super-low interest rates achieved one key outcome: encouraging Americans to borrow, spend, and help grow the economy after the Great Recession.

Last June, credit-card debt finally hit a new high. But the share of borrowers who make payments more than 30 days late is rising along with interest rates.

“That stands in stark contrast to the trend in delinquency rates on other forms of lending, which are either flat or falling,” Michael Pearce, a senior US economist at Capital Economics, said in a note on Monday.

"One explanation is that the surge in interest rates, which has been far sharper for credit card lending than for other forms of borrowing, has left a greater share of families struggling to make repayments," he continued.

The Fed is set next month to raise its benchmark rate for the seventh time since late 2015.

Some people are ditching credit cards in favor of cash, saving up, or passing on purchases. The number of credit inquiries within the past six months, a gauge of demand for credit cards, fell in the first quarter to a record low, according to the Federal Reserve Bank of New York.

Another possible reason so many people are missing credit-card payments is that unlike with auto loans and mortgages, the bank won't come knocking to repossess whatever has been purchased.

Though the 2008 recession was driven by a credit crisis, Pearce said this trend in cards was not going to crash the US economy, even if it worsens. Credit-card debt tallies to about $800 billion, less than one-tenth the size of the mortgage market in 2007 and about 6% of disposable income, he said.

"But we are increasingly concerned that, with broader market interest rates now rising sharply too, the rise in credit card delinquencies is a sign of things to come," Pearce said.

Missed credit-card payments may not hurt the economy, but they certainly hurt individuals. Creditors report late payments to the credit bureaus, and more than a third of a credit score is influenced by this history. A lower credit score means a riskier borrower, who could struggle to be approved for future credit lines or be charged higher interest rates.