Mangostar/Getty Images

- Simple interest is the interest applied only to the original amount of money borrowed or deposited, also known as the principal.

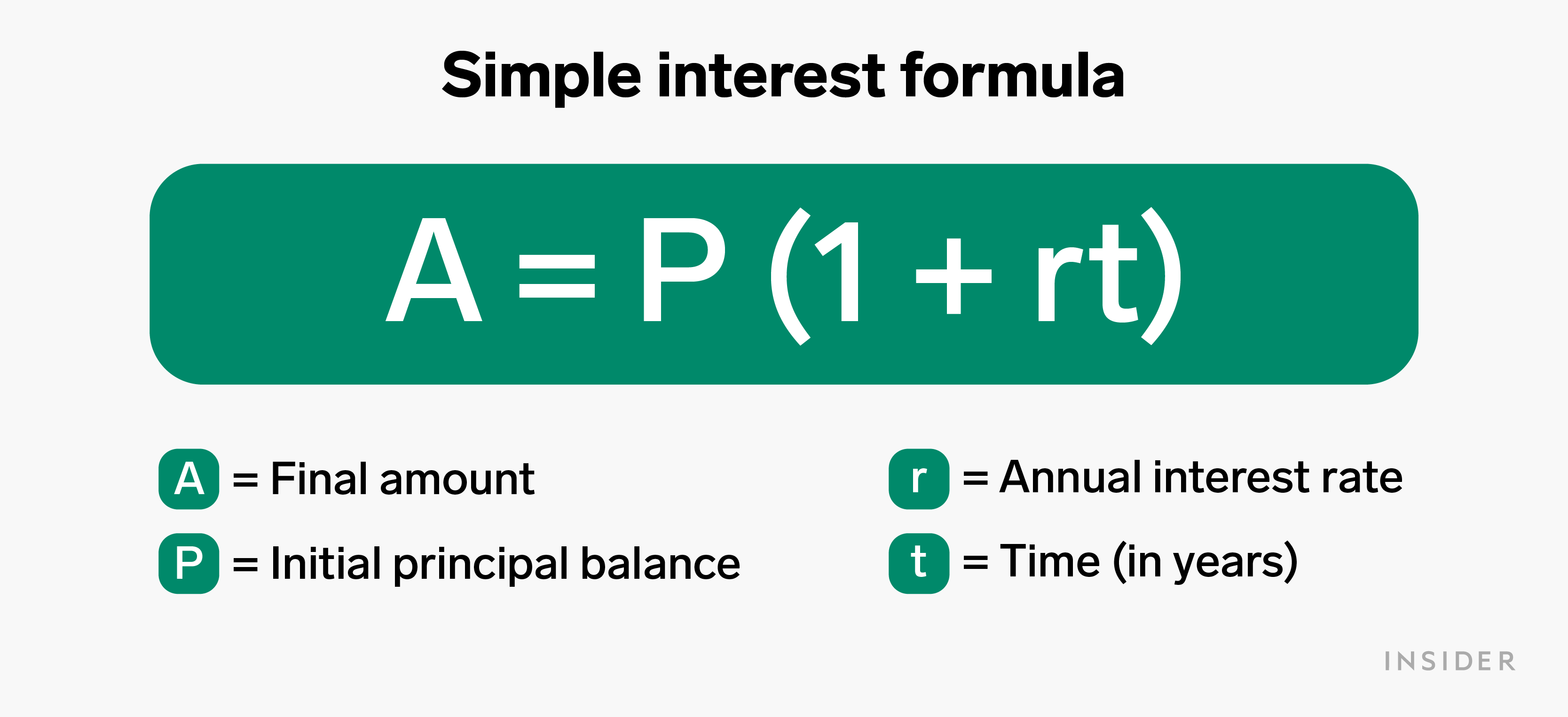

- It's calculated by multiplying the interest rate by the principal payment, then by the time (in years) you're investing your money.

- Unlike compound interest, simple interest does not accrue over time, making investments grow at a slower rate.

- Visit Insider's Investing Reference library for more stories.

They say money doesn't grow on trees, but one way to to make the most of what you earn is by paying attention to interest.

As far as financial concepts go, interest is one of the most important to understand. Essentially, it's the payment you receive when you lend (or deposit) money, as well as the money you pay when you borrow it.

Interest also comes in two forms: simple and compound. Simple interest is calculated based on an investment or loan's principal balance, which is the initial amount you put down or borrowed. And compound interest combines previously accumulated interest to the initial amount, sometimes referred to as "interest earned on interest."

Understanding simple interest and how it can affect your savings account or a potential investment is the first step in deciding whether it will be advantageous for your situation.

What is simple interest?

Interest is the fee attached to money, whether borrowed, loaned, or invested, and simple interest is the fixed rate that applies only to an investment or loan's principal balance. This type of interest calculation is considered simple because of how it's applied.

Simple interest is relevant to saving, borrowing, and investing, though it's typically most fruitful when borrowing, because it means your debt won't pile on over time.

Simple interest most commonly applies to short-term loans, like car loans, installment loans, personal loans, and some types of mortgages.

The first payment made on a simple interest loan covers that month's interest charge, with the rest going toward reducing the principal amount. Each month's interest is paid out in full, and any unpaid interest does not add up from one month to another like compound interest.

Simple interest can also affect how you invest and grow your money. It's interest earned only on the initial amount invested, or the principal balance. Investors earn simple interest on a steady basis, and it doesn't accumulate with time.

Savings accounts or certificates of deposits with this interest structure earn you a monthly interest income in exchange for making your money available for the bank to lend out.

How to calculate simple interest

The formula for simple interest is as follows:

Simple interest is often calculated on a daily basis, so it is most beneficial for borrowers who pay their loans early or on time every month. That way, they tackle the principal balance faster, which means the loan is paid off before its originally estimated date.

But if you pay your loan late every month, more of your payment goes toward interest. In that case, the total loan payment will exceed its original estimate, since you didn't pay the principal at its initially estimated rate.

Simple vs. compound interest

When borrowing money, simple interest is more advantageous for borrowers than compound interest, since it keeps overall interest payments lower.

On the flipside, lenders benefit less from charging simple interest than compound interest, because their money isn't compounding, or adding up, as it could be otherwise.

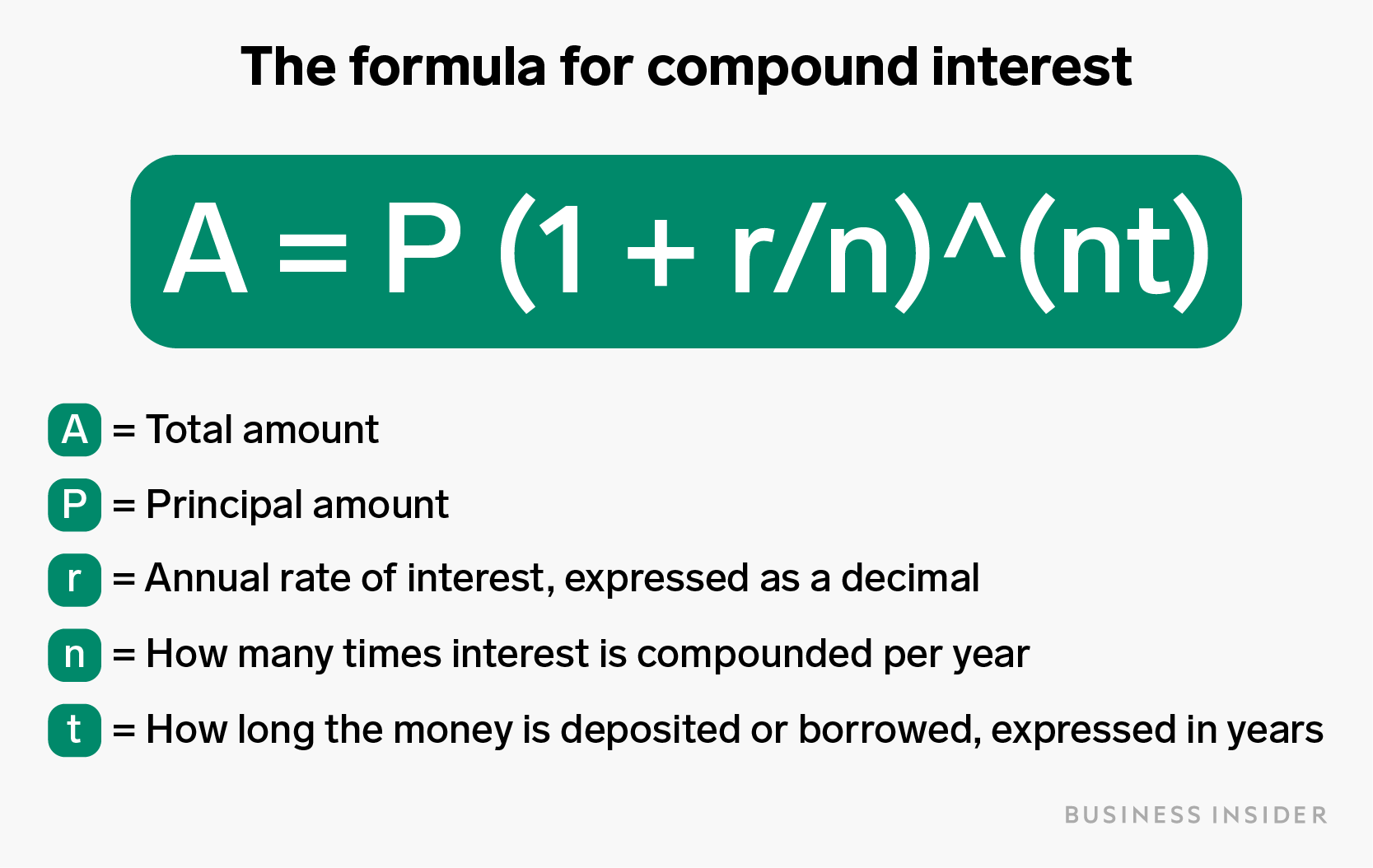

Compound interest combines the initial amount loaned with the interest that's been accumulated from previous periods. Thus, it's calculated based on both the principal amount and previously accumulated interest, and the formula is as follows:

Compound interest is a bit of a double-edged sword. It can be incredibly useful in generating investment savings and building wealth - but it can also cause some to spiral into debt if they borrow money that charges this type of interest and don't pay it off quickly or on time. That's why it's best to take advantage of compound interest when saving and investing rather than when taking on loans.

Simple interest is more commonly used for shorter-term transactions than compound interest, though it can also apply to financial arrangements without an established end date, like credit card balances.

Another difference between simple and compound interest? With simple interest, late loan payments subject the borrower to paying more money to cover the extra interest while maintaining the original principal balance. In contrast, late compound interest payments add a portion of the old interest to the loan, and new interest is calculated on top of whatever the borrower already owed.

How simple interest can work against you

So, when is simple interest better than compound interest? Well, that depends on whether you're the one borrowing or lending money.

Simple interest benefits the borrower, since it will cost less overall to pay off a loan that is not compounded over time. With each payment a borrower makes, the amount left to repay decreases the quicker they pay off the loan - which means less interest to pay back. For the lender, compound interest tends to be more beneficial since your interest itself earns interest, giving you more money in the end.

When you're looking to grow your money, simple interest might not be the way to go. An account with compound interest will accumulate money much faster, in the same way that it works against you when you're trying to pay off debt.

The financial takeaway

Simple interest is a straightforward way to calculate the interest that accompanies an investment or loan. It's based on the principal amount, or the money you agreed to put down or pay back at the start.

Simple interest differs from compound interest because the money does not accrue over time. It's found by multiplying the interest rate by the principal payment, then by the amount of time until it's paid.

It's best to use simple interest when borrowing money or paying off debt, and compound interest when lending, saving, and investing.