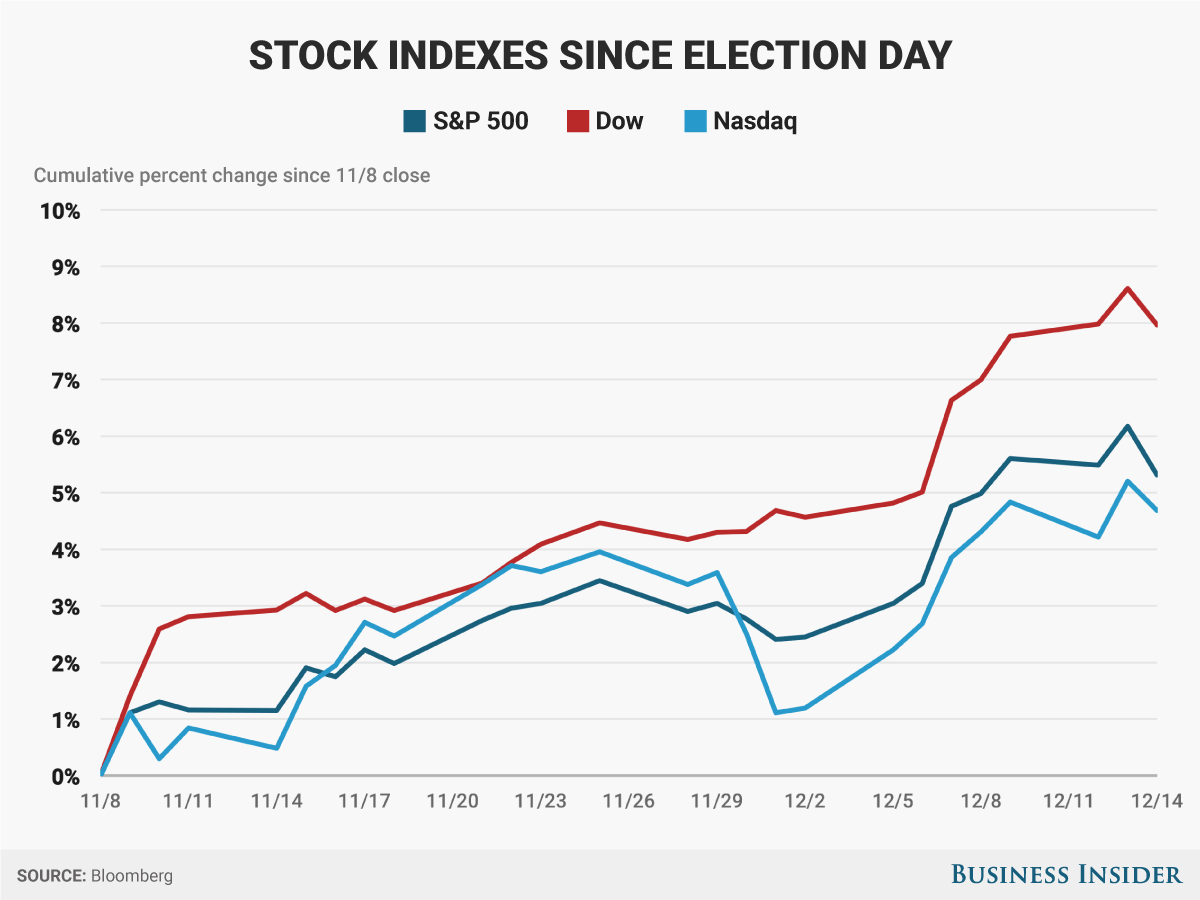

The stock market is set to end the year poles apart from where it started.

2016 started with the worst first 28-day performance ever for the S&P 500 Index. These days – ever since the US presidential election – it is jumping from new high to new high.

“It is a little scary to see such optimism,” said Randy Frederick, vice president of trading and derivatives at Charles Schwab.

“But at the same time, when I look out between now and the end of the year, I’m having a difficult time finding anything that’s probably going to derail this market outside of a black-swan event” which you can’t prepare for anyway, he told Business Insider in a telephone interview.

This market’s reversal is not uncharacteristic, as history proves that stocks usually rise. But they don’t rise in a straight line, and it will be after the current rally ends that some of euphoria of the last few weeks will be seen as a clear sign that this cycle is peaking.

It's not just the extreme bullishness. Much credit for the rally in stocks goes to President-elect Donald Trump's victory. He had been the unlikely winner, but investors and economists swiftly turned bullish on his plans to cut taxes, ease regulations and boost infrastructure spending. In short, they think Trump will be great for economic growth and company earnings.

But after stocks have run up so far, so fast, investors are likely to find that they were too enthusiastic about Trump administration's effectiveness, and that they underestimated the relative appeal of bonds over stocks.

'Really nobody was hedging'

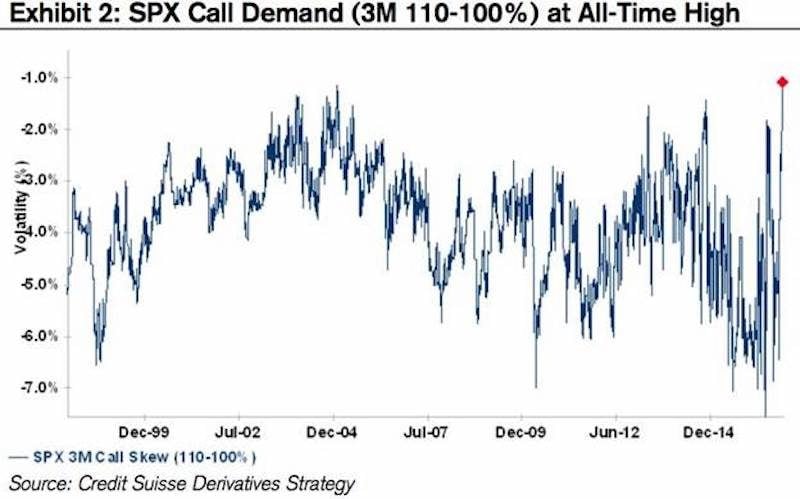

Outside of the all-time records being repeatedly broken, one marker of the euphoria can be seen in the derivatives market.

"The only thing I'm worried about is that it seems like nobody is worried about anything right now," Frederick said. That's based on his analysis of recent action in the options market.

He said virtually all equity put/call ratios - which compare the share of bets for a decline against bets for an advance - are in bullish territory.

Not only are investors not buying puts, they're buying more calls. According to Credit Suisse analysts, the price of call options that bet on a 10% rally in the S&P 500 recently rose to a record high.

"Really nobody was hedging the downside in this market," Frederick said." It's pretty unusual."

Overall options-market volume has surged in recent weeks, Frederick added, which is uncharacteristic of a period when stocks are going up.

Trumponomics

At the post mortem on this rally, the bullish bets on Trump's impact on the economy and corporate earnings will be front and center. Trump is promising the first sweeping corporate tax reform since Ronald Reagan was president, including incentives to encourage companies to repatriate capital parked overseas. He's also laid out an infrastructure spending plan that investors seem to be betting will boost the economy. Some of the so-called Trump rally reflects the expectation for higher earnings next year, said Wayne Wickler, chief investment officer of the retirement-services provider ICMA-RC.

The excitement over this may end though, when investors see the reality of Washington politics. As analysts contemplate how Trump's proposals could boost company earnings, they should "take into account that here in Washington DC, things just take longer than you would anticipate, than might happen in the private sector," he said.

"What is missing there is the calibration of timing to both implement and then have companies take advantage of a change in the landscape."

But the market's optimism is ultimately for good reason, he added. Notably, the expectation that the US economy will move away from monetary-policy support and towards fiscal policy, is a positive sign. It's usually hard to turn this tide on Wall Street, but Trump's win has managed to do this, he said.

"Even though I have a bit of a cautionary temperament in terms of the level of equities over the next twelve months, I wouldn't say it's a negative story," Wickler said. "I would say it's just one that probably has gotten a little ahead of itself."

A 'violent rotation'

While stocks have been rallying on expectations of a pro-business government, the very same factor has taken a toll on the bond market. Trump's win marked the moment when many investors began to call the end of the 30-year bull market in bonds - because they think his policies will be inflationary.

The rise in inflation expectations - characterized by stronger demand for US goods and accompanied by higher interest rates - siphoned money from bond funds to equity funds.

Bank of America Merrill Lynch characterized this as a "violent rotation." Its investment strategy team said in a note on Friday that $21 billion flowed into equity funds last week. That's the ninth largest amount ever. Meanwhile, $4.4 billion exited bond funds in a seventh straight week of outflows.

But there's a flip side to this swift move. The fall in bond prices, which raised yields to a three-year high in some durations, has put stocks in a position where they're expensive relative to bonds, according to Societe Generale's cross asset allocation team. In theory, that could be a reason for this violent rotation to start to reverse.

Another reversal could come from foreign investors from countries where bond yields are negative or near zero - highlighted by this chart from Deutsche Bank. Switzerland has negative yields - shaded in red - on all its bonds out to a duration of eight years.

But if more of the chart turns blue - indicating that yields on those bonds are going positive - some money managers are worried that things may end badly for stocks, said Torsten Sløk, Deutsche Bank's chief international economist.

"Ultimately, they may start to say 'maybe I shouldn't be buying all these risky assets in the US if I can get a higher return at home,'" Sløk said at a press briefing in New York on Thursday.