- Mike Wilson is Morgan Stanley’s US equity strategist. For a year he’s been one of the Street’s biggest bears.

- In early 2021, he called for 10% to 20% correction based on a “fire” and/or “ice” scenario.

- The “fire” scenario is currently underway, Wilson explains why the correction isn’t over and how to know when it is.

Morgan Stanley clients keep asking Mike Wilson: is it done yet? The correction in US stock markets, that is.

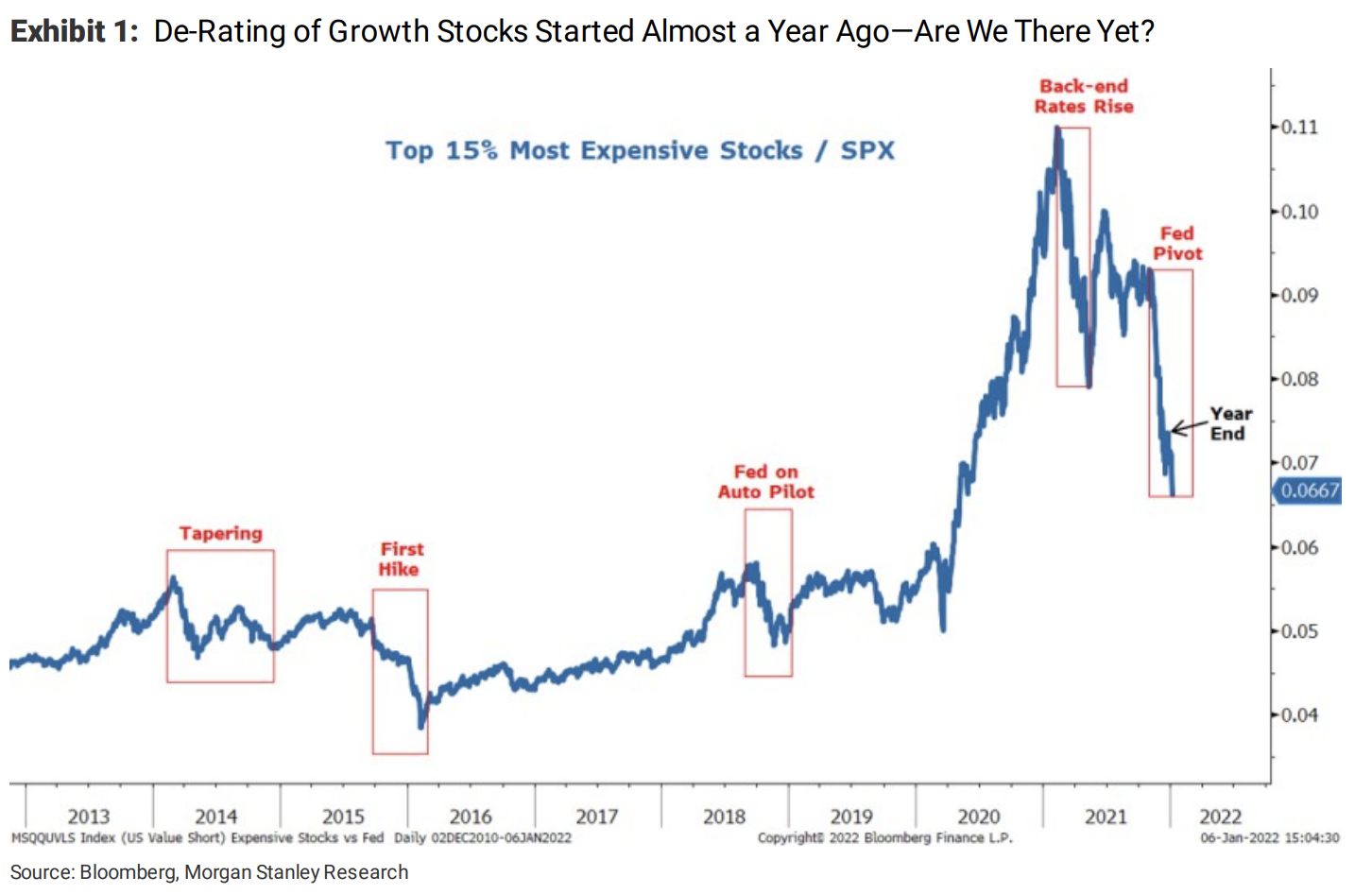

Wilson is the firm’s chief US equity strategist and according to his team, the most expensive stocks in the market were down around 30% in the last two months of 2021. Year-to-date, that same group is down an additional 10%.

Last year, Wilson became recognized as one of the most bearish strategists on Wall Street, with a call in early 2021 that the S&P 500 index could correct 10% to 20% due to a “fire” and/or “ice” scenario.

A “fire scenario” is one in which red-hot inflation causes the Federal Reserve to tighten monetary policy aggressively, while an “ice scenario” is one in which economic growth decelerates, hitting stock valuations and earnings expectations.

The investment world sits up and listens when Wilson makes a correction call. He’s been right on his last two big calls.

By the end of 2021, the S&P 500 returned 29% and hit a high of 4,787 on the final day of the year. Wilson's correction never materialized at an index level. However, under-the-surface moves were already taking place.

Wilson kept his conviction on the outlook. At the start of this year, his "fire" scenario ignited when the release of Federal Reserve's December meeting minutes highlighted the central bank's more hawkish tone toward monetary policy.

The S&P 500 and NASDAQ indices are down near 3% and 5%, respectively this month, with growth stocks down 4%, versus a 9% gain in their value peers.

Tech stocks have been especially hard hit. According to wealth manager RIA Advisors, nearly 40% of stocks in the Nasdaq are now down more than 50% from their 52-week highs and only 13% of days have seen more stocks cut in half since 1999.

So as Wilson's clients ask: is there more to come?

"This is having a disproportionate impact on expensive growth stocks, as it should, but the real determinant of how long and deep this correction lasts will be growth," said Wilson, answering the question in a January 10 research note.

Investors are now entering a tighter monetary policy environment and this is going to mean more uncertainty at the index level, he added.

Even with the "fire" scenario underway, there is still the potential for a further correction to take place.

As a comparison, Wilson uses the 2013 "taper tantrum", when the Federal Reserve announced it would wind down bond purchases, and valuations for the broader S&P 500 actually increased.

"After all, Fed tightening is a good sign for growth and evidence that its policy has been successful," Wilson said. "In fact, that was exactly the argument we made in 2013 and why we were very bullish on that tapering episode."

But this environment is different for two reasons: valuations are much more stretched than in 2013 and growth was accelerating, he said.

In this current environment, he expects 10-year real yields to reach a point where they are at least positive. Using 10-year inflation-adjusted rates as a proxy, the equity risk-premium - a valuation metric that adjusts for the absolute level of rates - is now as low as the tech bubble in the 1990s, he said.

"In short, we've never seen stocks this expensive for the overall market, which means valuations are likely to come down more before we're through with this correction," Wilson said. "This is exactly our call for 2022, and why we think it's not done playing out."

In addition to this, Wilson still sees the "ice" scenario playing out, with economic and earnings growth decelerating.

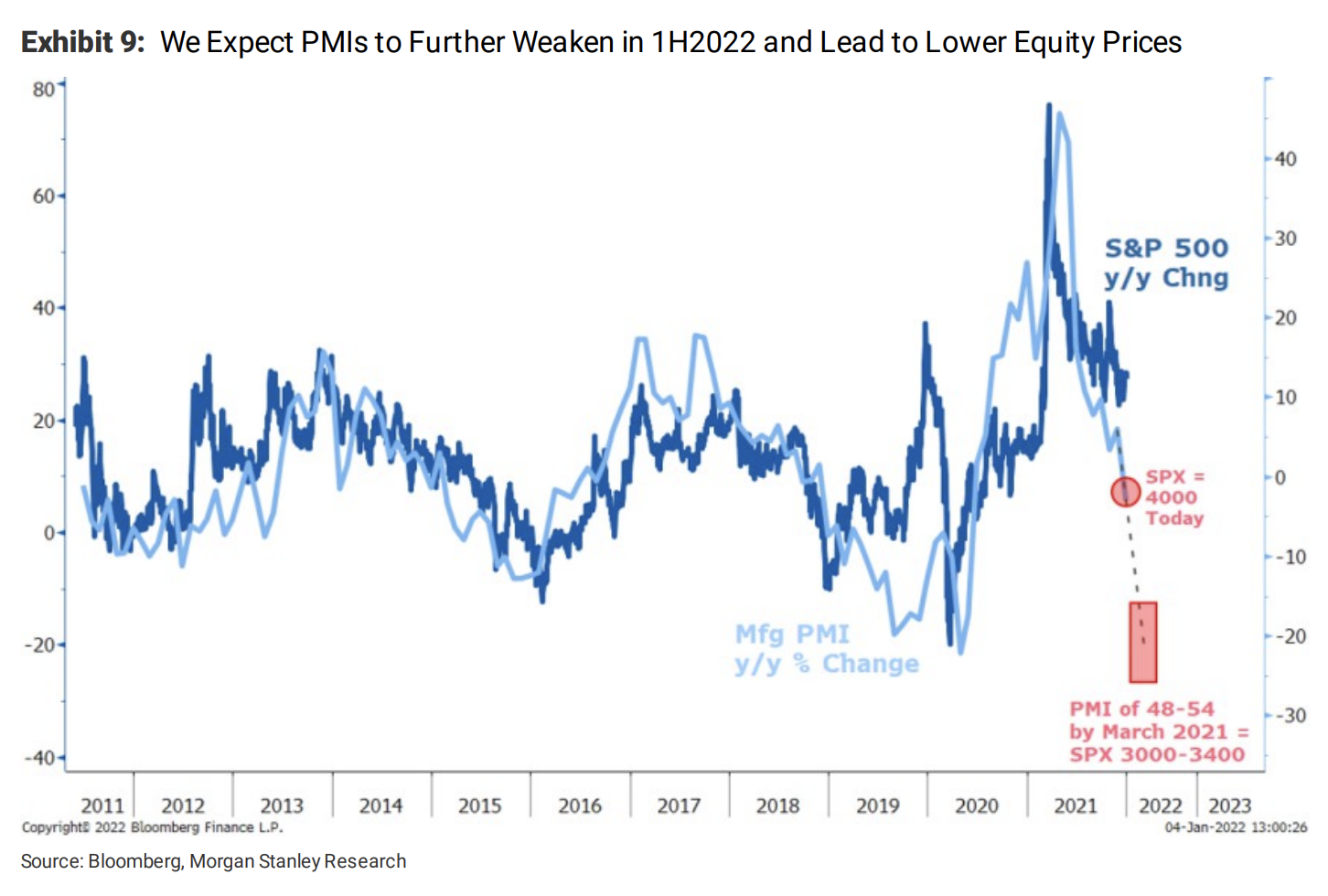

There are two key drivers behind the growth of stocks, Purchasing Managers Indexes (PMIs), a measure of economic activity, and earnings revisions, Wilson said.

Wilson expects a reversion in extraordinarily high PMIs.

"Our guess is that by the spring of this year, we will see a manufacturing PMI in the low 50s, if not slightly worse given how high it got this time—every action entails a comparable reaction," Wilson said.

Earnings revisions also have a strong positive correlation to stock prices and are being used as a gauge of growth acceleration and deceleration by Wilson. If earnings are adjusted downwards in the face of slowing growth, this could also be another factor in the correction of stock prices.

"From weak breadth to extreme leadership in quality stocks, we think a deteriorating economic and earnings situation that is likely worse than most investors expect is being depicted within market internals—i.e., PMIs, economic and earnings growth will accelerate further than investors expect during the first half of 2022," Wilson said.

Investor positioning

Historically, this style of environment has meant defensive leadership is a key area for investors to be positioned in going forward, Wilson said.

He's recommending a barbell of large cap defensive quality stocks, with small-cap value stocks with an overweighting toward healthcare, REITs and financials.

Indicators for the end of the correction

1) Software stocks

This is a category that's borne the brunt of the correction thus far. In Wilson's eyes, these stocks are reacting to deteriorating earnings revisions relative to the S&P 500.

"Conversely, it does look like relative revisions are trying to bottom so if this can fully reverse during 4Q earnings season, so should the stocks,at least on a relative basis assuming rates stabilize, too," Wilson said.

2) Investment grade credit spreads

Investment-grade credit spreads tend to lead the rally in stocks, Wilson said. However, he notes the last two highs made by the S&P 500 were not confirmed with record-low premia in investment-grade credit spreads.

"Given the importance of credit spreads to equity valuations via the risk premium channel, we would simply chalk this up as yet another thing to watch for the all clear sign that this correction is over," Wilson said.