After demystifying the multi-billion digital marketing industry in a presentation last year, the investment bank LUMA Partners has just released its annual State of Digital Marketing presentation.

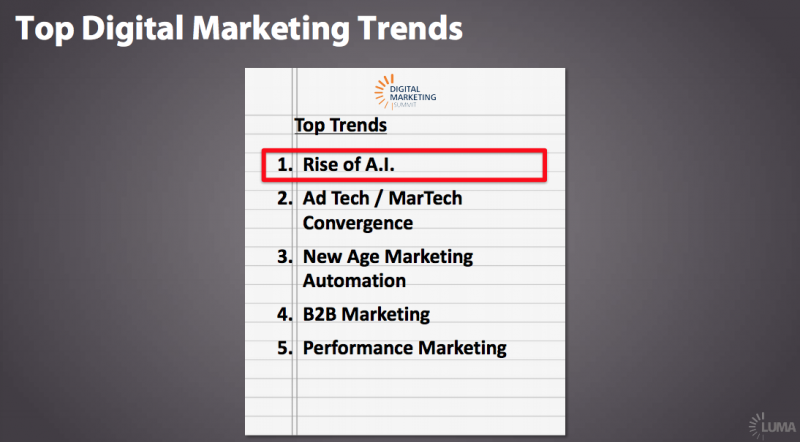

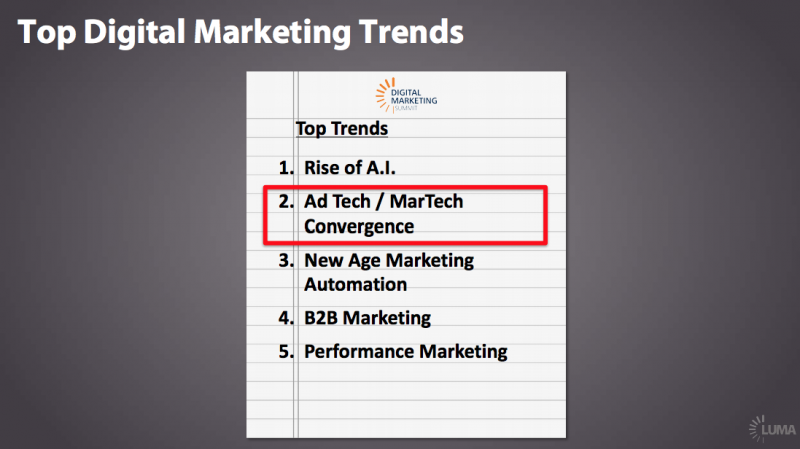

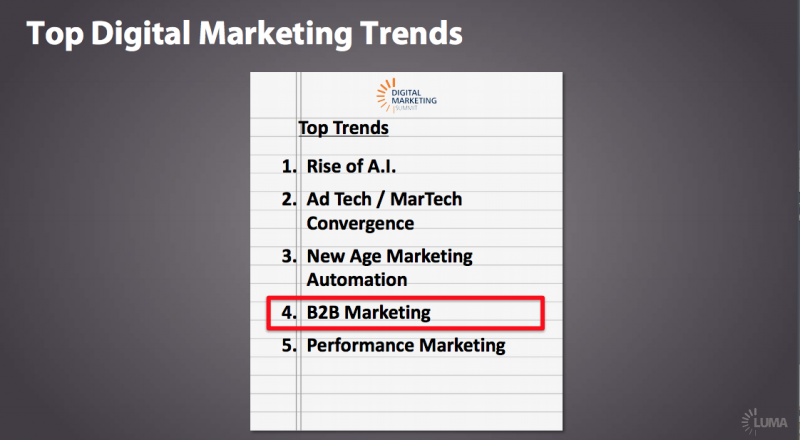

This year it covers LUMA’s views on the market, five industry trends – including the rise of artificial intelligence – and the future of the ecosystem with a specific focus on digital marketing.

The investment bank has allowed Business Insider to publish its annual presentation, again.

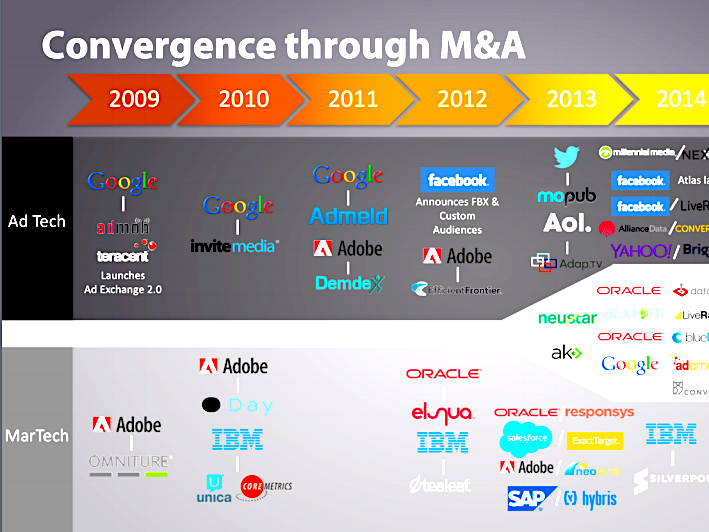

This year you can expect to learn a lot about the convergence of the ad tech (marketing) and martech (technology) industries through a lot of M&A activity.

LUMA presents our annual State of Digital Marketing, which covers our views on the market, industry trends, and the future of the ecosystem with a specific focus on digital marketing. We hope you enjoy it.

Foto: source Luma

Meet the Senior LUMA Team.

Foto: source LUMA Partners

Foto: source LUMA Partners

LUMA's singular industry focuses on the intersection of Media, Marketing, and Technology; the sectors of digital content, ad tech, and martech all seen through the lens of mobile.

Foto: source LUMA Partners

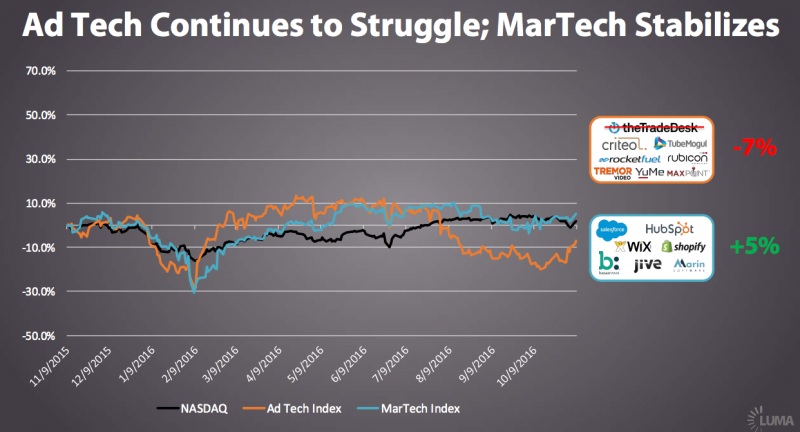

After a rocky start to the year, martech stock prices have stabilized. Ad tech stocks show stronger performance when including the industry’s newest entrant, The Trade Desk, which began trading publicly in September.

Foto: source LUMA Partners

On an “apples-to-apples” basis, excluding this year’s new entrant The Trade Desk, we see the ad tech sector in negative territory year-over-year.

Foto: source LUMA Partners

Beyond the stock prices, when we divide by revenue and look at multiples over the same period, we note stable stock prices but growing revenues yield declining multiples for martech. Including The Trade Desk, which is currently trading well above its peers, multiples in ad tech appear unchanged.

Foto: source LUMA Partners

Excluding The Trade Desk, ad tech multiples are down almost 50% while revenues continue to grow meaningfully for both ad tech and martech.

Foto: source LUMA Partners

Revenue growth remains the primary driver of multiple across both ad tech and martech.

Foto: source LUMA Partners

Since our last DMS West a year ago, we have seen only one IPO in the ad tech and martech spaces. The Trade Desk priced in September and is still hovering around its $1 billion valuation, a rare bright spot for public ad tech companies and perhaps a signal of more to come.

Foto: source LUMA Partners

Last year we noted a palpable change in sentiment in the funding environment and this change remains evident in the data with venture capital funding down significantly in martech, and even more so in ad tech.

Foto: source LUMA Partners

That said, differentiated companies are still finding capital. In fact, over 30 industry leaders have each raised at least $20 million since the last DMS West.

Foto: source LUMA Partners

The one real bright spot in the market: M&A! We’ve seen almost a score of scaled strategic exits in the last year.

Foto: source LUMA Partners

Interestingly, valuations paid for these scared strategic exits have been at a meaningful premium to current public market valuations.

Foto: source LUMA Partners

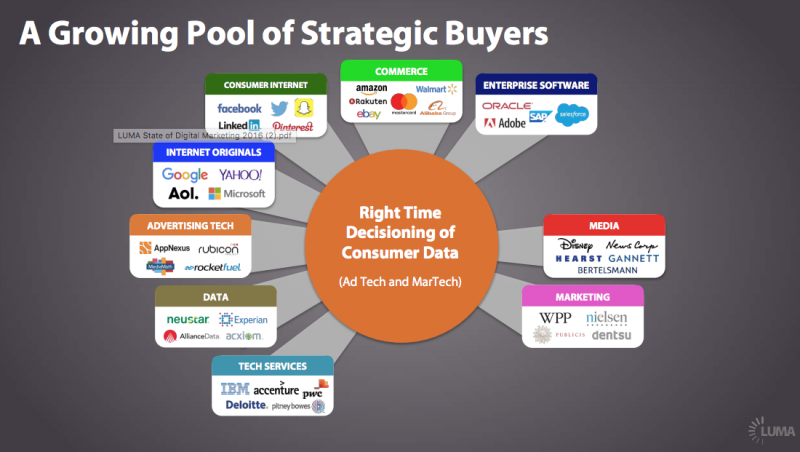

What is driving this activity? A growing pool of strategic buyers. We see continued activity from the usual suspects like the enterprise software and ad tech, but a number of new entrants are also making an active push into this space.

Foto: source LUMA Partners

Telcos have been very active as they aim to monetize their larger customer bases and enter the fast growing digital advertising market. They have already made a number of significant transactions just this year alone. LUMA expects more to come in the near future.

Foto: source LUMA Partners

Private equity has also entered the space. With predictable revenues, high operational leverage, and healthy margins, some companies in the industry fit the financial profile that intrigues financial buyers.

Foto: source LUMA Partners

Lastly, international buyers, most notably from China, have been very acquisitive this year.

Foto: source LUMA Partners

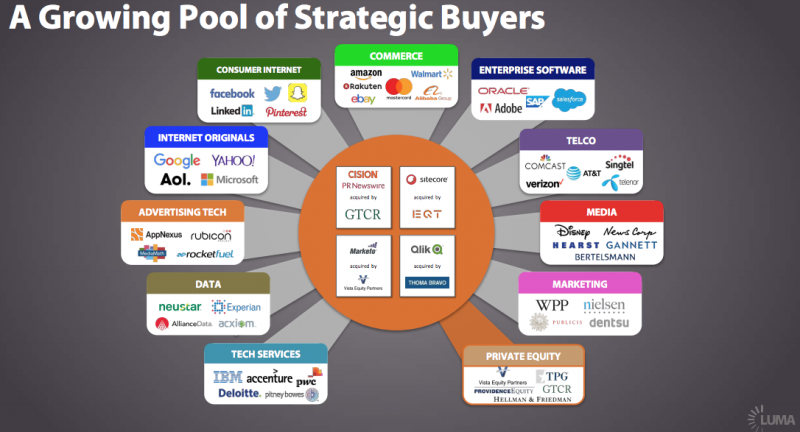

Interestingly, we have seen private equity buyers step up for martech assets, paying multiples we typically associate with strategic buyers.

Foto: source LUMA Partners

And Chinese buyers have come on strong in ad tech with a number of scaled exists just in the last quarter (e.g. Smaato, Media.net, and AppLovin).

Foto: source LUMA Partners

Foto: source LUMA Partners

Foto: source LUMA Partners

In the past 6-12 months there has been increasing focus and awareness on artificial intelligence (AI). However, as Forbes suggested, we are now in a period of skepticism (“disillusionment and chaos”) of AI as the market experiments with AI to determine whether it provides a benefit – or not. But we firmly believe that we will be entering the “amazement” phase very soon.

Foto: source LUMA Partners

The AI market is still very early. The below projection reminds us of the programmatic advertising market in 2010 when marketers were first experimenting with the technology. When the industry saw the effectiveness of programmatic, the market took off – and it is now about 2/3 of the display advertising market. We believe the same dynamic will occur with AI as it gets applied more to ad tech and martech and transforms the industry.

Foto: source LUMA Partners

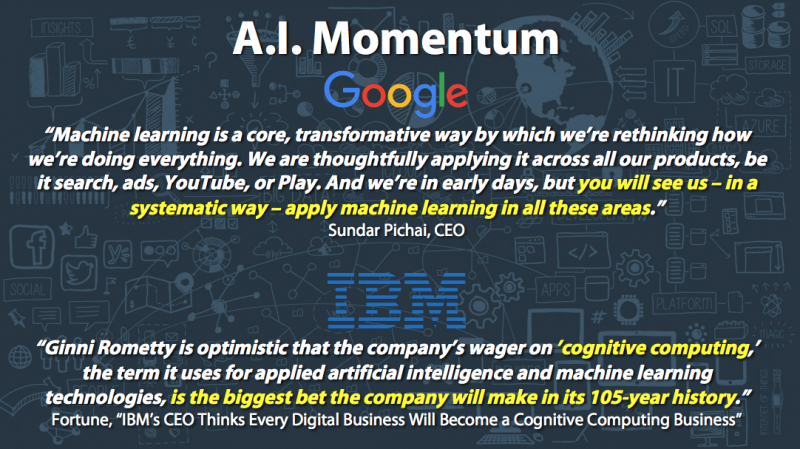

We aren’t the only ones bullish about AI. Tech giants like Google and IBM are making significant investments in this technology. Google is planning to apply machine learning across all its products, and IBM is making the “biggest bet” in its history around cognitive computing.

Foto: source LUMA Partners

Even the President is weighing in. AI will be applied across a multitude of industries: automotive and transportation (self-driving cars and long-haul transportation), health care, research and - our focus area - marketing and advertising.

Foto: source LUMA Partners

AI has been applied to the marketing industry for some time, but mainly at the "edges," meaning narrow, specific use cases. For instance, in display advertising, AI has been applied to bid or creative optimization, and predicative analytics have been utilized for real-time content insertion for websites and email. We believe that AI will now move towards the "core" to coordinate activities across these channels. More on this later in the presentation…

Foto: source ZUMA Partners

Foto: source LUMA Partners

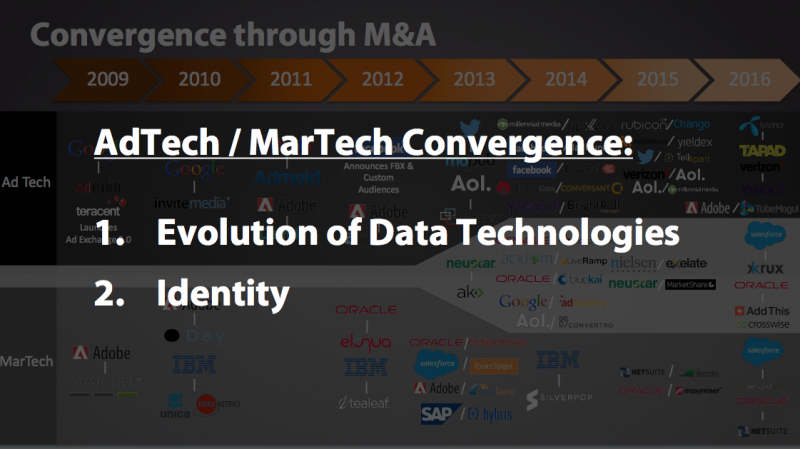

In the past ad tech and martech were very distinct industries, with little connection between the two. As ad tech evolved into data-driven advertising and martech into data-driven marketing, we have seen the data layer become the conversion point for these industries. This consists of DMPs, online / offline data, and planning and attribution systems.

Foto: source LUMA Partners

Two sub-trends that are part of the larger ad tech/martech convergence trend are: 1) the evolution of data technologies, specifically DMPs, and 2) the rise of "identity" solutions as a critically strategic capability in the market.

Foto: source LUMA Partners

When Demdex, one of the earliest DMPs, launched in 2010, it was primarily a cookie management platform for display advertising for publishers. In recent years, the capabilities and use cases of DMPs have expanded. DMPs now have additional functionality such as data analytics, tag management, and robust mobile data management. And use cases have expanded from just display advertising to areas such as web personalization and A/B testing.

Foto: source LUMA Partners

It has long been church and state between CRM systems and DMPs, separating personally identifiable information (PII) from anonymous data. But we are now starting to see these data sets blend within platforms such as DMPs. It will be especially interesting to see how Salesforce integrates Krux once that acquisition closes, and whether they combine PII and traditionally "anonymous" data sets.

Foto: source LUMA Partners

The DMP has been known as one of the key software platforms to enable targeting for digital advertising. With the evolution of DMP capabilities and use cases, it now sits "at the centre of the marketing cloud" as the "hub of enterprise intelligence."

Foto: source LUMA Partners

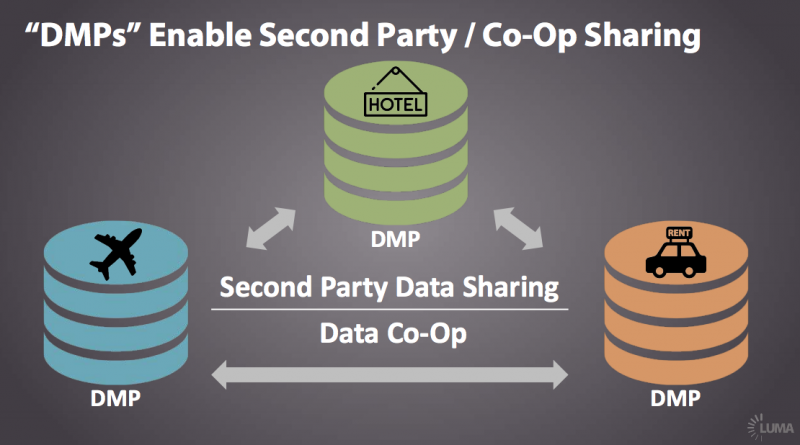

Despite the evolution of the DMP, we are still in the very early innings of this industry. Large enterprises are only just beginning to implement DMPs and managing their first-party data assets effectively. One trend we believe will emerge is a dramatic rise of second-party data sharing among companies in complimentary industries as well as the growth of data co-ops. Adobe is pursuing this opportunity aggressively with its Audience Marketplace.

Foto: source LUMA Partners

If you observe the rise of the marketing clouds, you will notice that they have been very focused on consolidating point solutions (Phase 1) – which makes sense. As mentioned earlier, DMP capabilities and use cases have expanded. ESPs such as Exact Target have also evolved, adding SMS and social channels to their platforms. But across all the marketing clouds, the various point solutions are still fairly channel-focused with only minimal integration.

Foto: source LUMA Partners

We believe the Marketing Clouds will now aggressively move to “Phase 2,” which is to “orchestrate” activities across channels in order to optimize the customer experience. This orchestration layer will include both rules-driven and AI approaches to help marketers accomplish true 1:1 marketing — sending the right message to the right person at the right time through the right channel. This will drive further convergence of ad tech and martech.

Foto: source LUMA Partners

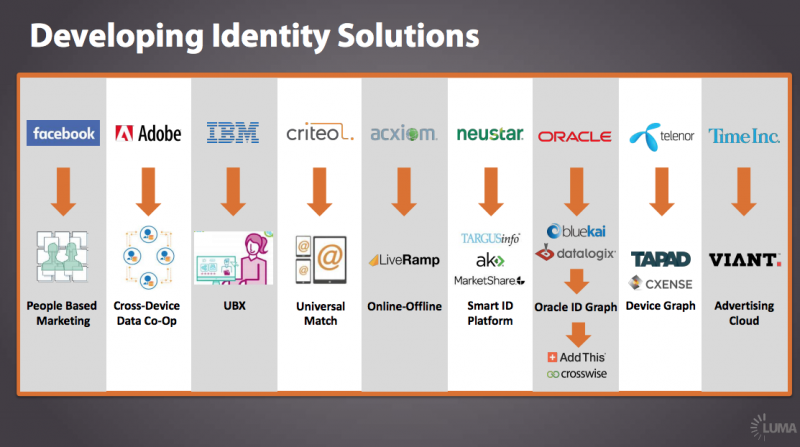

“Identity” is a key industry focus since it's critical to being able to coordinate the customer experience. Identity offerings have been advancing rapidly, with incumbents furthering their offerings while others have entered the market. We have long talked about Oracle being the most active in building its identity solutions with its “Data Cloud”, but there are other major players building robust identity solutions, such as Adobe, Neustar and Acxiom.

Foto: source LUMA Partners

The “identity graph,” which organizes multiple data sets – purchase, demo, behavioral, digital IDs and location – for each individual, has emerged as a key identity offering. The identity graphs not only enable sophisticated targeting for marketing, but also feed into planning and measurement applications as well. We will continue to see significant investment in identity graphs from the marketing clouds and startups alike.

Foto: source LUMA Partners

Foto: source LUMA Partners

Predictive marketing platforms emerged a few years ago and are being adopted by e-commerce companies to enable 1:1 personalization. These systems combine data from e-commerce platforms (providing purchase history for each user), browsing data (short-term browsing behavior) and other systems. Combined with a predictive analytics engine and a product feed, these platforms then coordinate personalized content across channels.

Foto: source LUMA Partners

Mobile marketing automation companies emerged due to dynamics in the app economy: 1) consumers are downloading fewer apps, 2) it is expensive to acquire new users, and 3) most apps are free and app publishers struggle to monetize users. These platforms create profiles on each user, and coordinate triggered messages: in-app, push notifications and emails. Some also help optimize the app with analytics and A/B testing.

Foto: source LUMA Partners

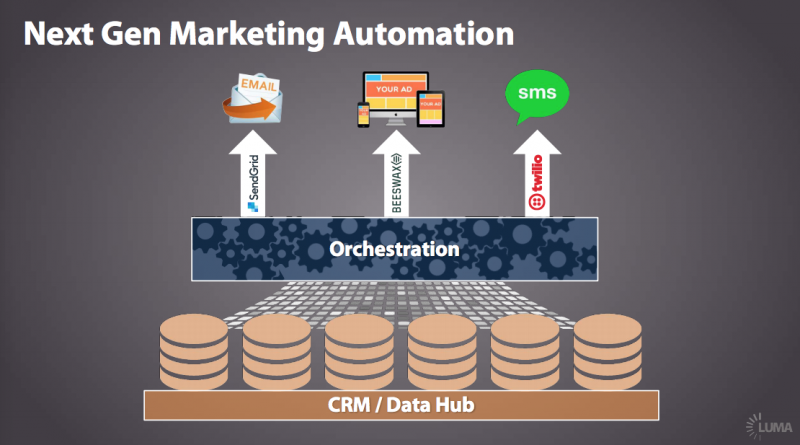

What do “predictive marketing” and “mobile marketing automation” companies have in common? They both have a data hub / CRM system at the core, and also provide the orchestration for interactions with each consumer. Unlike the Marketing Clouds, with point solutions that need orchestration, these have orchestration at the core. If they need to add a new channel, such as email or SMS, they generally use OEM systems such as SendGrid or Twilio.

Foto: source LUMA Partners

Foto: source LUMA Partners

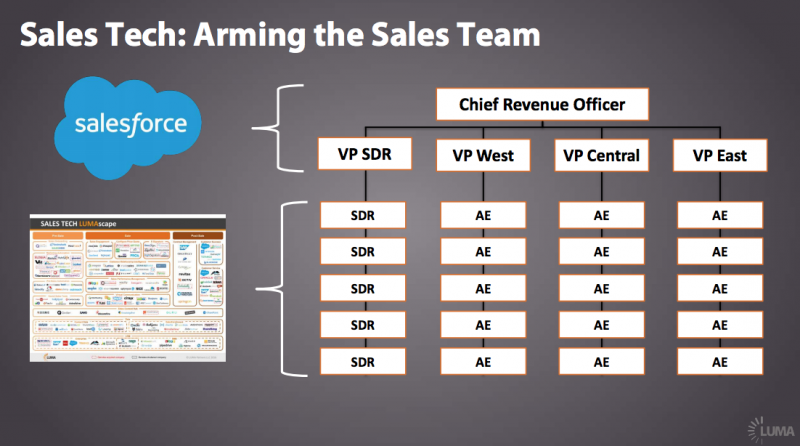

We have talked about account-based marketing (ABM), delivering the right message at the right time to the right account, and predictive analytics, which folds into ABM. They both have grown dramatically in the last year. The next key trend to watch is the convergence of martech and sales tech. While ad tech and martech convergence applies to B2C marketers, martech and sales tech convergence applies to B2B marketers with direct sales teams.

Foto: source LUMA Partners

There is now a burgeoning ecosystem of companies focused on building tools for key steps and workflows within the entire sales process. We have created the sales tech LUMAscape to help map out the growing ecosystem, which you can find on www.lumapartners.com.

Foto: source LUMA Partners

CRM systems like Salesforce are focused on the management layer of an organization, not the individual sales person. In the last couple of years we have seen an increasing number of startups emerge that are focused on making the actual account executive or SDR more effective at his / her job. Investors have recognized this as well, as we are seeing more VC investment and growth in this area.

Foto: source LUMA Partners

Foto: source LUMA Partners

During the early days of performance marketing, the industry was filled with very questionable businesses from "toolbar" companies to "incentive" sites. Not only did these companies not drive incremental sales, but they also drove spam, adware and other problems. When performance marketing is mentioned today, many still conjure up images of these questionable practices.

Foto: source LUMA partners

But what defines performance marketing today? Google and Facebook.

Foto: source LUMA Partners

In May, Morgan Stanley reported that Google and Facebook captured over 85% of incremental digital ad spend in Q1 2016. This is a very tough dynamic for the rest of the ecosystem in which companies are battling over the remaining 15%. A recent analysis concluded that Google and Facebook actually captured over 103% of the growth in the first half of 2016. In other words, the rest of the industry may actually be shrinking.

Foto: source LUMA Partners

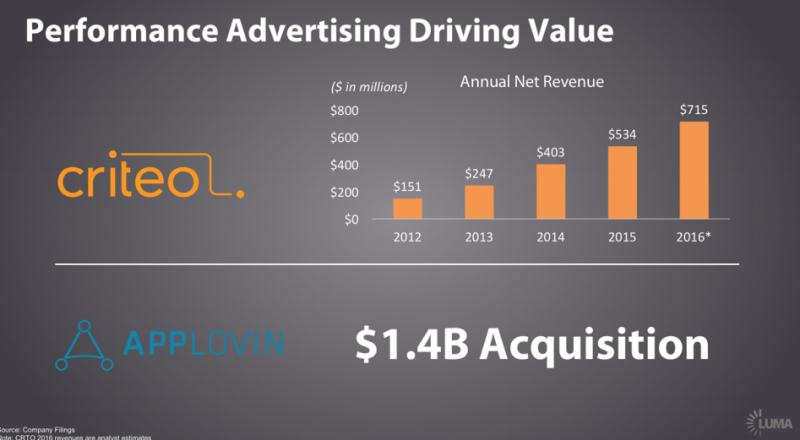

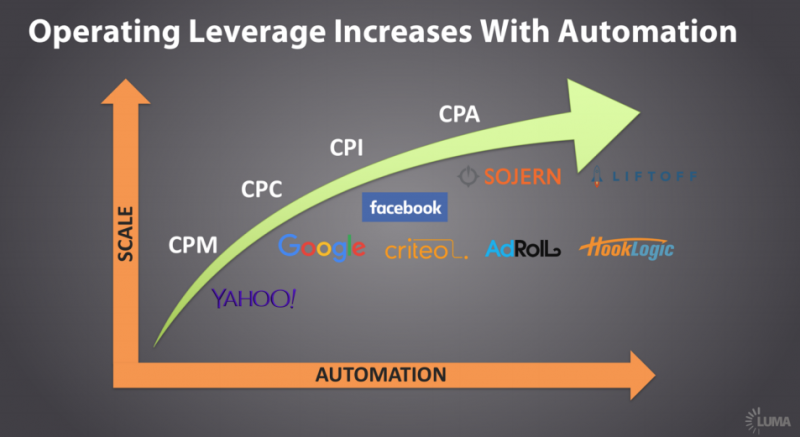

But not all is lost. Marketers want performance and if a vendor can deliver it they will continue to spend. Criteo has built a scaled business by servicing advertisers directly and using cost-per-click pricing. Customers spend up to the efficient frontier, just like search, resulting in always-on ad spend. AppLovin has built a tremendous business with staggering growth and profitability through developing terrific technology and using pricing that aligns with its customers.

Foto: source LUMA Partners

We have witnessed the evolution of pricing models from CPM to CPC to CPI, and ultimately CPA, driving the action marketers are trying to achieve. By aligning pricing with its customers’ desired outcomes (and developing robust technology to deliver those outcomes), leading performance marketing companies are able to create terrific scaled, predictable and profitable businesses.

Foto: source LUMA Partners

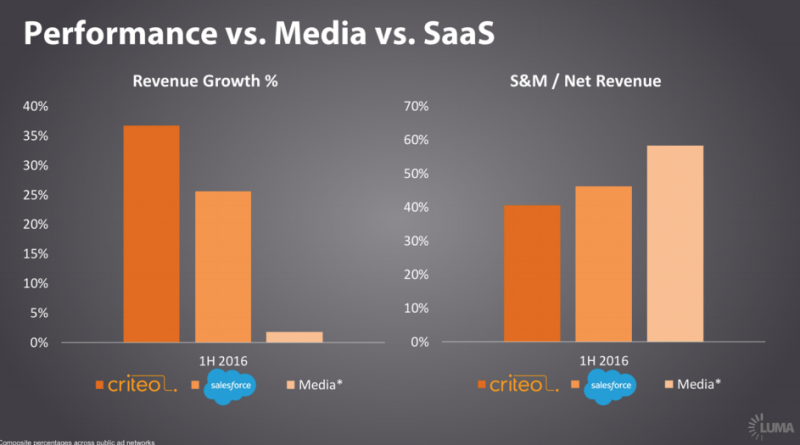

We hear some people say that Criteo is just an ad network. However, let’s compare Criteo to the public ad networks and also to the most successful SaaS (software-as-a-service) company — Salesforce. In the first half of 2016, Criteo had higher revenue growth with lower sales and marketing (S&M) cost as a percentage of revenue — highlighting its predictability of revenues and high operating leverage. The public ad networks, in contrast, generally are not growing and have higher costs in general.

Foto: source LUMA Partners

LUMA Institute is the division that incorporates our research, content and events initiatives. The mission of the LUMA Institute is to provide education, insights and market development to all constituents of the digital ecosystem. We partner with media, marketing and technology companies to provide advice and education at leadership offsites and customer events on a customized basis. If LUMA can help your organization sort through this complicated and dynamic sector, contact Gayle Meyers at [email protected].

Foto: source LUMA Partners