- Exchange traded funds have grown 500% in value since 2008 to $4 trillion. Deutsche Bank’s Long-Term Asset Return Study examines chance that ETFs could be the trigger of the next major crisis.

LONDON – Financial crises have all sorts of triggers

The 2008 crisis started with the collapse of the sub prime mortgage sector in the USA and wild speculation in the tech sector in the 1990s caused the dot-com bubble to burst.

While crises are hard to spot by their very nature, that hasn’t stopped Deutsche Bank strategist Jim Reid and his team attempting to categorise all the events that they believe could be catalysts for the next big one.

We’ve already written about the potential for Italy’s fragile political and economic situation to trigger a new crisis, as well as the risks a breakdown in Brexit talks would pose – but there is one more threat in Deutsche Bank’s report that we feel is worth looking at.

That is "(A lack of) Financial Market Liquidity…and changing market structure," with the rise of exchange traded funds (ETFs) of particular note.

An ETF is a passive fund which tracks an index, rather than an active investment, and seeks to outperform a given index through frequent buying and selling of individual investments.

ETFs have seen a boom in the ten years or so since the last crisis, with growing numbers of investors opting to invest in ETFs rather than actively-managed funds, which are associated with higher fees, and have offered lower returns over the last decade.

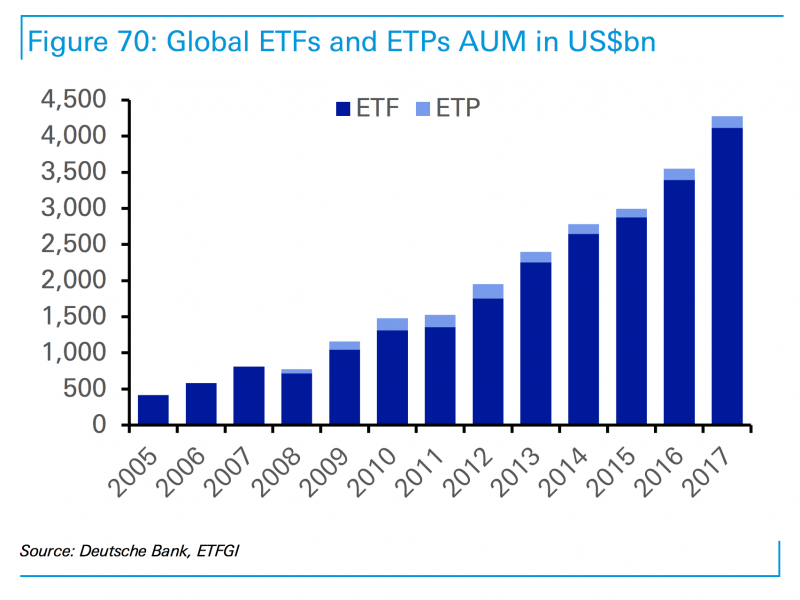

Growth in the amount of money invested in ETFs is "extraordinary," Reid and his team say. "Putting the numbers in perspective, including ETPs (which make up a much smaller percentage), the global AUM of exchange traded products (all asset classes) is now over $4tn. This compares to around $800bn or so in 2008."

Here is the chart:

ETFs have grown rapidly, but their resilience has not really been tested by any significant market hardship, leading some observers to question if the sector will be able to cope with a substantial market correction should one come in the near future.

This is especially true when considering that some believe ETFs can distort the markets by encouraging investors to put money into big companies - simply because they're big names - regardless of their market fundamentals (things like price-earnings ratios, return on equity etc.)

Here's Reid's explanation (emphasis ours):

"One argument is that passive investing naturally favours large caps when picking constituents based on factor style (for example momentum, growth etc). In theory this means that the biggest companies are getting bigger, regardless of fundamentals.

The concern therefore being that these companies are perhaps more susceptible to overvaluation and the gap between the small/mid to large caps also widening. This could potentially mean that risks are amplified when you see a big market correction, which arguably ETFs haven't yet been tested with yet."

ETFs did get something of a test around 18 months ago, Reid and his team write, when a drop in the oil price caused a sell-off in the high yield bond markets. Some believe that ETFs made that sell-off worse, while others believed ETFs helped provide liquidity to the market, preventing a worse correction.

"In reality," Deutsche Bank's argument goes "ETFs and ETPs have not yet been fully tested in a sustained bear market. So the real test could be when we see the next downturn and these products are faced with heavy redemptions. This will be particularly paramount for less liquid asset classes."

The ETF industry is yet to see how the asset class performs in a sustained bear market. We're currently in the second biggest bull market since the Second World War, so we might be waiting a while.

"The emergence of more and more exotic niche ETFs only complicates the landscape," Deutsche Bank says.

"The products warrant close attention particularly in the context of their surge in popularity for retail investors and as with any market still somewhat in its infancy, the real test is probably still to come."