- It has become trendy to insist that everyone ignore the bond yield curve, and how darn flat it looks.

- The curve (allegedly) measures how risky investors perceive things to be, and a bond yield curve inversion can predict recessions.

- Recently, the curve has been distorted by central banks’ bond-buying programs, which have artificially made the curve flatter than it might have been. So the curve is a bad signal, some people say.

- “This time it’s different,” a UBS economist told clients (in a tongue-in-cheek way). He called the curve signal a “myth.”

- Here’s why you should continue to obsess about the curve: It can signal risk despite central bank activity.

LONDON – For an economic indicator that is allegedly not a reliable signal for impending recessions, people sure are talking about the flattening of the bond yield curve a lot. Recently, it has become trendy to insist that everyone ignore the yield curve. “The yield curve is not an indicator of impending doom! Ignore it!,” they say. Of course, whenever an important person insists that the rest of us ignore something, that just makes me more curious about it.

The problem is that whenever you do look at it, it makes you think.

Hmm.

That curve sure is flat.

The yield curve, in plain English

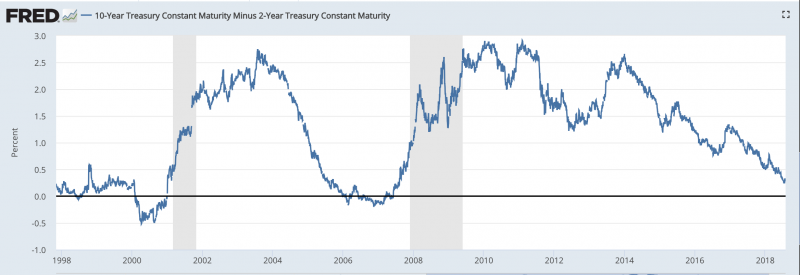

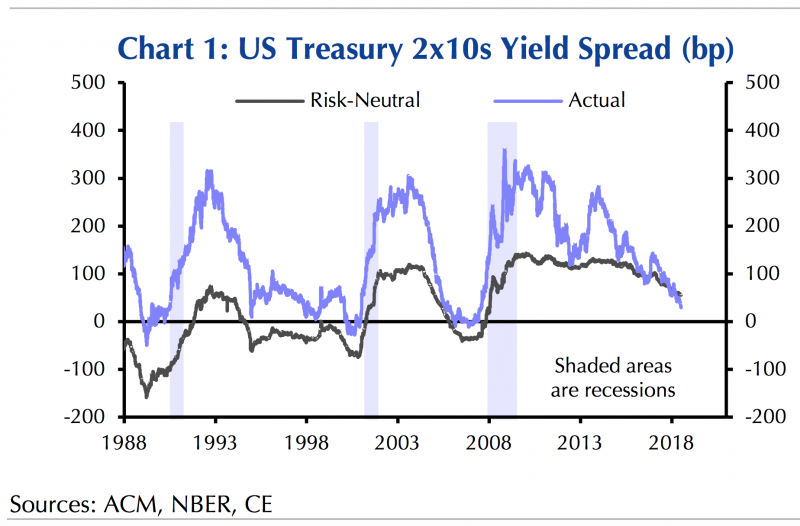

The bond yield curve has in the past been a signal of an impending recession. When the interest yield on the 10-year US Treasury bond becomes the same as the two-year bond, recessions have often followed. The "curve" is the line that plots the difference between them over time. Right now that line is trending toward zero, or flat. If the line goes below zero - an "inversion" in which the yield on the two-year bond would be greater than the 10-year - that traditionally signals something is very wrong in the market.

Why? Because a flat or negative yield curve suggests investors believe keeping your money in short-term bonds is more uncertain than bonds that pay off a decade from now. Think about it. That position doesn't make sense. Why would you be more certain about 2028 than 2020? Thus, when the curve inverts, it signals something very risky is happening in the near-term asset markets.

Hey presto, recessions follow.

"This time it's different"?

Right now some loud voices are insisting that this time it's different. This time the curve is wrong, they say.

Chairman of the US Federal Reserve Jerome Powell helped this view along when he testified to Congress in mid-July that the curve's flatness was not the most important thing about it. Rather, he said, it is what the curve says about the neutral rate of interest that really matters. The "neutral rate" is a complicated concept and we don't need to go into it here. But the upshot is, he didn't say that the yield curve was per se doing anything bad.

Others have gone further.

Last week, before he left on a vacation, UBS global wealth management chief economist Paul Donovan sent a note to clients calling the yield curve signal a "myth" and, knowingly - jokingly - tempting fate, he said "This time it's different":

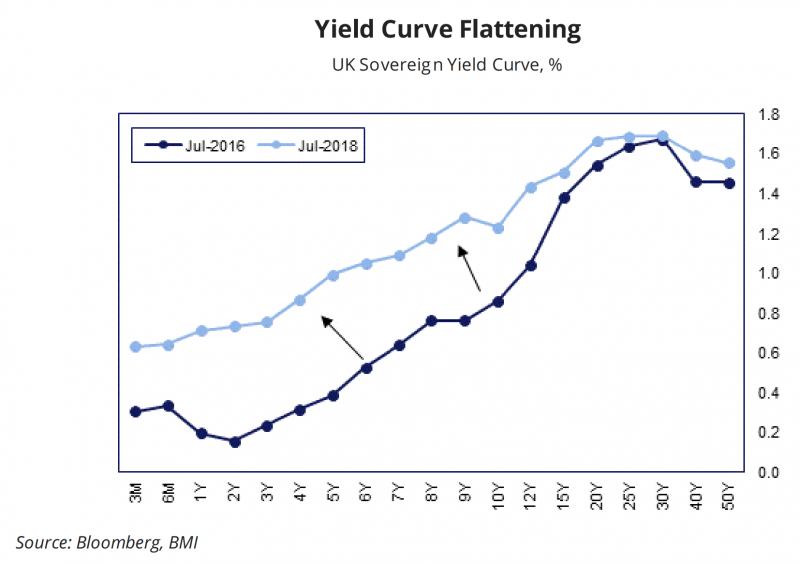

"Before looking at why this myth is not true today, there are two very obvious reasons not to believe the story. The myth suggests that bond dealers know more about the future than anyone else. Indeed it suggests bond dealers know more about the future than economists. That does not seem very likely. The myth also suggests that the US yield curve has some magic ability to forecast the future, but other country's yield curves do not. The UK yield curve has inverted for years at a time with no recession. The Japanese yield curve has not inverted since 1991, in spite of one recession after another. ... If bond yield curves can predict, they should be able to predict everywhere. They do not."

Here's the UK version of the yield curve ... it's getting flatter too.

"It's kind of like, I don't believe in torture, because torture is immoral, but also, a tortured prisoner is going to lie to you"

Who else do we have?

There is David Kelly, Chief Global Strategist of JPMorgan Asset Management, who told Business Insider earlier that the curve was distorted because central banks, since the financial crisis of 2008, have pumped cash into the economy by buying loads of bonds. That has pushed up the price of long-term bonds, lowering their yield. (When prices go up, buyers get lower yields because the final return on a bond is fixed. Thus prices and yields move in opposite directions to each other on bonds.) Because those quantitative easing programs are structurally built-in to the bond market right now, and because central banks don't play around in the market like investors, the long-term bond market is a bad signal for anything, he says:

"Central banks have been buying long-term bonds like never before, and they're basically sitting at the long end of the yield curve, and that's distorting it. It's kind of like, I don't believe in torture, because torture is immoral, but also, a tortured prisoner is going to lie to you. The yield curve is being tortured by central banks, and is going to tell us lies. Now, it doesn't mean there couldn't be problems in the future, but we're going to need a better measure of what's going on than the yield curve," he said.

And it is difficult to ignore Mohamed El-Erian, the chief economic adviser at Allianz, who, writing for the Financial Times recently, said "yield curve messaging about the prospects for nominal growth should be taken with a grain of salt - especially when many commodities continue to point to robust global activity."

These are all smart people ... right?

And yet ...

These are all smart people. And they are right that central bank buying activity has distorted the curve in a way that they may not have in the past. But the curve doesn't only measure the holdings of central banks.

The curve reacts to a lot of things. For instance, it reacts to how investors feel about risk in other assets. If investors think the world is suddenly going to become very risky, very soon, they will pile into bonds they think are safe. Why put your money in two-year bonds if the reason you are switching to bonds is that you don't know what the heck is going to happen over the next two years? In an uncertain world you might conclude that 10-year bonds are a better bet.

There is a ton of uncertainty in the world. North Korea. Chinese debt. Trump's trade wars. Brexit. Italian debt. Right now much of the economic and political world looks as if it is composed entirely of uncertainty. It's bad today. Surely we'll have fixed the world in 2028?

So the flat curve could be signaling a bit of that.

And although some smart famous people think the yield curve is broken, there are some equally smart not-so-famous people who are watching it very carefully. CLSA's Christopher Wood pointed out to clients recently that aside from the Fed's Powell, the rest of the Fed is still watching the curve for recession signals: "The FOMC minutes of 12-13 June reflect a clear lack of consensus on this yield curve issue. To quote from the original: 'A number of participants thought it would be important to continue to monitor the slope of the yield curve, given the historical regularity that an inverted curve has indicated an increased risk of recession in the United States.'"

Central banks can distort the curve and the curve can still signal impending doom

Here is the nightmare scenario, as sketched by Andrew Cates of Nomura in a note to his clients. You can assume that the central banks are leaning artificially on the long-term end of the curve, and his theory still says the curve is a danger signal. He argues that the world might enter a period of "stagflation" - that is, low growth and high inflation. That is a tough world for a central bank, because normally you'd want to print more cash to fuel growth but you can't do that without worsening inflation. In such a scenario, banks might choose to fight inflation first (emphasis ours):

"A stagflation scenario - the combination of negative growth surprises and positive inflation surprises - would not be constructive for risk assets. That's particularly if policymakers - in the face of a trade-off between low growth and high inflation - opt to combat rising inflation. In light of positive output gaps, rising core inflation and pro-cyclical US fiscal policy, this might not be unreasonable. This could invoke a tighter policy response, hampering longer-term growth expectations and speed up curve inversion."

So, yeah, central banks can distort the curve and the curve can still signal impending doom.

Given that, I'm going to keep watching the curve.

The rest of you can do whatever you like.