In a note highlighting the “catastrophic distortions” caused by central bank quantitative easing, Albert Edwards, the Societe Generale über-bear strategist, says that the US is actually doing it worse than other countries.

In Wednesday’s note, Edwards highlighted the work of his SocGen colleague Andrew Lapthorne, who contrasted the quantitative easing programs from the Federal Reserve and the Bank of Japan.

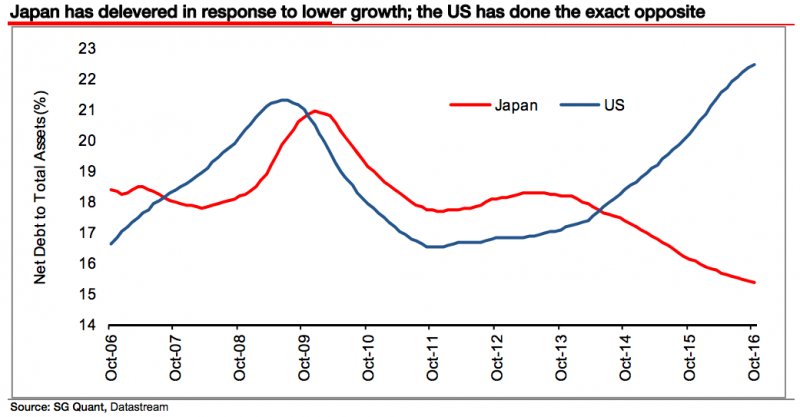

The Fed, Lapthorne noted, allowed firms to borrow easily, and as their debt increased they bought back their own stock instead of kick-starting economic growth with capital investments.

On the other hand, the Bank of Japan simply bought Japanese equities directly, keeping the burden of QE on the central bank instead of allowing the companies to run up their debt.

Thus US corporations have a heavier load of debt as compared with their total assets, whereas Japanese companies have actually seen their leverage decline compared with total assets.

"This difference is important," Lapthorne wrote. "In a market downturn, equity market losses will lead to the BOJ having to mark to market its equity holdings at a lower price. In the US, lower equity markets will lead to balance sheet disruption with the inevitable job losses and cuts in capital spending."

Edwards, in his assessment of Lapthorne's point, went even further, calling the leverage among corporates "nuts."

In fact, Edwards said that Japan has done fairly well in using QE to combat its own economic stagnation. The weakness of the yen as a result of its direct purchase method allowed corporate profits to rebound without taking on too much debt. In turn, the inflation rate of imports ticked up and could have created a wage growth cycle.

Unfortunately, the BOJ allowed the yen to strengthen this year, ruining the cycle - it has "blown their chance of reviving the economy," Edwards wrote.

Japan still had a chance, however, since it had not allowed its financial markets to run out of control like the US. Edwards cited Leo Lewis of the Financial Times, who said 55% of Japanese corporations have more cash on hand than debt, while less than 20% of S&P 500 companies do. Thus it appears Japan has put itself in a more advantageous position in the event of a possible economic downturn.

So with high price-to-earnings valuations in the US and less cash-to-debt, it would appear that America is set up for a steeper fall than Japan's market.

"And with valuations where they are which equity market do you think QE has set up to collapse in the next recession?"